Merchant of Record: A SaaS Guide to Global Sales & Scale

Ayush Soni

Founder, Revcover

On this page

- Introduction The Global Sales Dilemma

- Why founders choose it fast

- The part most teams miss

- What Is a Merchant of Record

- The two transaction structure

- What the customer sees

- What the money flow tells you

- The Core Responsibilities of an MoR

- What the MoR actually owns

- Why finance leaders care

- The hidden operational truth

- Pros and Cons of Using an MoR for SaaS

- The real advantages

- The margin problem most guides ignore

- The branding invisibility problem

- My recommendation

- MoR vs Alternatives A Clear Comparison

- Payment Model Comparison

- What this means in plain English

- The MoR Decision Framework for Your Business

- Ask the finance questions first

- Then ask the customer experience questions

- Don't ignore downstream workflow friction

- My decision rule

- Conclusion Next Steps for Your Payment Strategy

- Three next steps I'd recommend

You've started selling outside your home market. Revenue looks good. Finance is nervous. Support is forwarding emails about invoices, taxes, refunds, and card statement confusion. Product wants to keep launching. Nobody on your team wants to become an expert in VAT, GST, PCI DSS, chargebacks, and local compliance rules.

That's the moment when Merchant of Record vendors show up with a clean promise: let us take the transaction risk and operational burden so you can keep selling globally. For many SaaS companies, that pitch is attractive for a reason. It solves a real problem.

But founders usually evaluate an MoR too narrowly. They look at tax compliance and faster market entry, then stop there. That's a mistake. If you run subscription software, your payment model doesn't just affect checkout. It affects refunds, statement descriptors, cancellation saves, payment recovery, and renewal trust. In other words, it affects the part of the business where margin is won or lost.

Introduction The Global Sales Dilemma

The global sales problem usually doesn't start with strategy. It starts with friction.

A buyer in another country wants to pay in their local currency. Finance asks who's collecting tax. Legal asks who is liable if a regulator asks questions. Engineering asks whether the current billing stack can support local requirements. Support asks why the customer's bank statement shows a name they don't recognize. The founder asks why a software company is suddenly doing international commerce operations.

That's why many SaaS teams move toward a merchant of record model. It gives you a shortcut. Instead of building and owning every part of the selling infrastructure yourself, you hand the legal sale to a provider that sits in the middle and takes responsibility for the transaction.

That sounds clean, and sometimes it is.

Why founders choose it fast

An MoR is appealing because it turns a long list of operational burdens into a vendor relationship. That matters when your team is small, your expansion plan is aggressive, and you don't want finance and engineering buried in payment operations.

The usual reasons are straightforward:

- Compliance relief: You don't want to manage tax calculation and remittance market by market.

- Liability transfer: You'd rather not be the party handling every chargeback, refund, and regulatory edge case.

- Faster expansion: You want to sell globally without setting up local entities just to accept payments.

Practical rule: If your team wants global revenue without building a global payments function, an MoR is the fastest path.

The part most teams miss

The MoR decision doesn't stop at compliance. It changes the unit economics of retention and the trust signals customers see after purchase.

If your cancellation flow relies on pauses, downgrades, targeted discounts, or card-update recovery, the payment model can either support that machinery or erode it. That's the issue most glossy MoR guides skip. They talk about selling internationally. They don't talk enough about protecting margin after the initial sale.

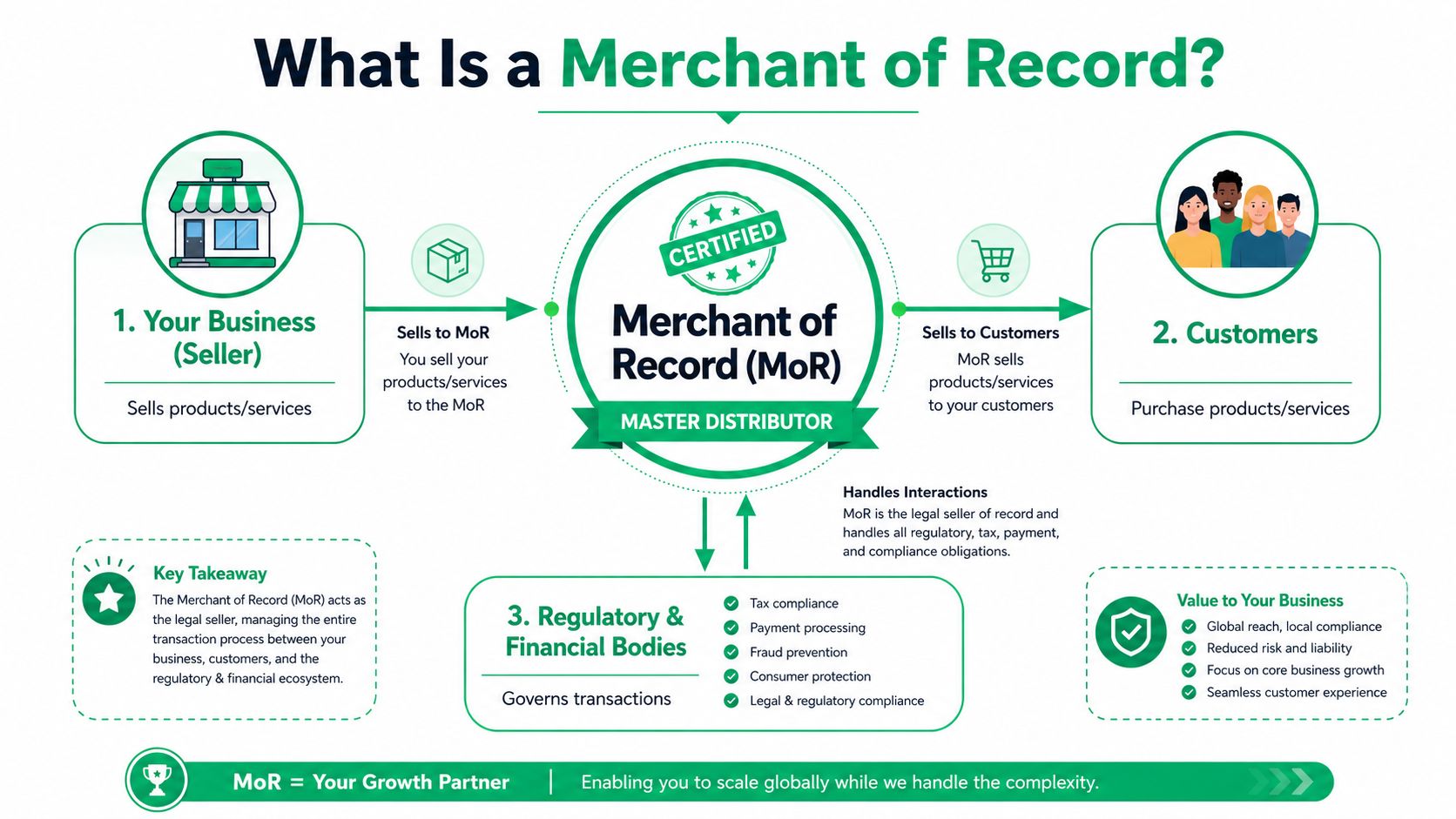

What Is a Merchant of Record

A merchant of record is the legal seller in the transaction. Not the software company that built the product. Not the payment processor moving money. The MoR is the entity that sells to the customer and takes responsibility for that sale.

The easiest way to understand it is to think of the MoR as a master distributor for digital commerce. Your SaaS company provides the product. The MoR stands between you and the buyer, handles the sale, collects the money, manages the transaction obligations, and pays you after deducting relevant taxes or fees.

The two transaction structure

This model works because there are two distinct transactions in each sale. According to Invoiced's explanation of the merchant of record model, first your business transfers ownership of its goods or services to the MoR provider, and then the MoR transfers that ownership to the end buyer. The customer pays the MoR directly, and the MoR later pays your business after deducting relevant taxes or fees.

That legal structure matters more than the label.

It means the MoR is not just helping you process a charge. It is acting as buyer to your company and seller to your customer. That's why the MoR can collect and remit sales tax, VAT, or GST and carry the transaction liability in a way a simple processor doesn't.

What the customer sees

When you use an MoR, the customer typically sees the MoR as the seller in the payment trail. That can include receipts, invoices, and the descriptor on the card statement.

For early-stage teams, that can feel like a minor branding compromise. It often isn't. If the customer expects your product name and sees a third party instead, support tickets rise and trust can weaken. I'll get to that commercial cost later, because it matters more than most founders think.

What the money flow tells you

If you want the plain-English version, use this checklist:

- Your company provides the software

- The MoR makes the legal sale

- The customer pays the MoR

- The MoR remits taxes and handles the transaction obligations

- Your company receives payout net of relevant deductions

A merchant of record is not “Stripe plus tax.” It is a different commercial structure.

That distinction is where good decisions start. If you misunderstand the structure, you'll underestimate the downstream impact on reporting, retention design, and customer communication.

The Core Responsibilities of an MoR

Once you sign with an MoR, you're outsourcing much more than checkout plumbing. You're handing off a stack of financial, legal, and operational responsibilities that would otherwise sit with your own team.

What the MoR actually owns

Stripe explains the distinction clearly in its overview of merchant of record responsibilities. Unlike a standard PSP such as Stripe that only processes transactions, an MoR takes on full liability for the transaction, including tax compliance, reporting, and regulatory obligations, while handling end-to-end payment flows from checkout localization to consumption tax remittance.

In practical terms, that means the MoR usually handles work like:

- Tax collection and remittance: Sales tax, VAT, or GST is collected at the point of sale and remitted by the MoR.

- Chargebacks and disputes: The MoR deals with the messy part when customers challenge charges.

- Refund operations: Refund policy execution and transaction handling often sit with the MoR.

- Compliance obligations: This includes standards and processes tied to secure payments and regulatory screening.

- Currency and localization mechanics: The MoR supports global transaction handling across markets.

Why finance leaders care

From a CFO or RevOps seat, the fundamental value is risk transfer. If you build this yourself, you need internal controls, specialist knowledge, reporting discipline, and a team that can keep up as rules change. If you outsource it, you reduce that internal burden but give up a degree of control.

That tradeoff is acceptable for many SaaS companies. It's often smart in the early and mid stages. But don't confuse “outsourced” with “free.” You still need internal visibility into how refunds, disputes, taxes, and statement descriptors affect your revenue operations.

A good example is bank-based payment collection. If your team is also evaluating non-card payment rails, it helps to understand the operational differences before bolting them onto a global billing setup. This guide to accepting ACH payments is useful because it highlights how payment method choice changes reconciliation, failure handling, and customer experience.

The hidden operational truth

The MoR removes burden from your org chart. It doesn't remove consequences from your business model.

When a vendor owns liability, they also shape your payment experience.

That's why founders need to ask operational questions early. Who controls refund timing? Who decides how descriptors appear? Who owns the support path when a customer doesn't recognize a charge? Those aren't side questions. They sit directly on the revenue line.

Pros and Cons of Using an MoR for SaaS

Most MoR writeups stop after the upside. That's incomplete advice. For SaaS, the pros are real, but the downsides show up later in finance, retention, and customer trust.

The real advantages

Let's give the model credit where it deserves it.

An MoR can dramatically simplify global selling. You don't need to stand up every compliance layer internally before entering new markets. Finance gets relief. Engineering avoids building edge-case billing logic too early. Legal exposure is reduced because the MoR becomes the liable party for the transaction.

For a founder trying to keep headcount lean, that's a big operational win.

Three benefits usually matter most:

- Speed to market: You can start selling internationally faster than if you build and own the stack yourself.

- Lower internal complexity: Tax handling, dispute workflows, and payment compliance move out of your day-to-day operations.

- Cleaner focus: Teams can spend more energy on acquisition, product, and customer success.

The margin problem most guides ignore

Now the part that should make every SaaS operator slow down.

The MoR fee structure can hurt you most when you're trying to save a customer, not when you're trying to acquire one. According to 2Checkout's merchant of record guide, 34% of SaaS companies using MoR for global sales report a 15-20% increase in net revenue leakage during churn recovery because MoR fees are applied to discounted save offers, not just gross sales. The same source says this can erode 2-3x more margin than standard PSP models during aggressive retention cycles.

That is not a rounding error.

If your retention engine uses discounted renewals, save offers, or rescue campaigns, percentage-based MoR economics can turn a “saved customer” into a weak-margin customer much faster than operators expect. This is one reason finance teams should model MoR cost against the full subscription lifecycle, not just new bookings.

If you want a better finance lens on how recurring revenue should be interpreted operationally, this piece on deferred revenue definition is worth reviewing alongside your payment model assumptions.

A retention offer that looks smart in product can look terrible in gross margin once MoR fees hit the discounted transaction.

The branding invisibility problem

There's a second cost, and it's less visible until support or renewals expose it.

When the MoR's name appears where your customer expects your brand, trust can slip. This matters more in B2B than many teams admit. Finance buyers, procurement teams, and admins notice statement descriptors and invoice names. If those signals don't match the vendor relationship they think they have, they hesitate, escalate, or fail to renew cleanly.

That's the branding invisibility paradox. The infrastructure gets simpler for you while the purchase feels less direct to the customer.

My recommendation

Use an MoR if speed, compliance relief, and reduced liability are the main priority. But don't approve it on those benefits alone.

Before you sign, model these two questions:

- What happens to gross margin when your save offers are discounted?

- What happens to trust when your brand is not the merchant name customers see after purchase?

If you don't answer both, you're evaluating only half the business case.

MoR vs Alternatives A Clear Comparison

An MoR is one payment model, not the default truth of global commerce. You can also use a payment facilitator like Stripe, build and operate as your own merchant, or sell through reseller and marketplace structures. Each option changes who owns liability, who handles taxes, and who controls the customer-facing payment identity.

Payment Model Comparison

| Criterion | Merchant of Record (MoR) | Payment Facilitator (e.g., Stripe) | Direct / Be Your Own MoR | Reseller / Marketplace |

|---|---|---|---|---|

| Legal liability for the sale | MoR provider holds transaction liability | Your business typically retains liability for the sale | Your business holds full liability | Marketplace or reseller often holds liability based on structure |

| Tax collection and remittance | Usually handled by the MoR | Usually your responsibility | Fully your responsibility | Often handled by reseller or marketplace under its model |

| Who appears on the customer statement | Often the MoR or MoR-aligned descriptor | Usually your business name or configured descriptor | Your business | Reseller or marketplace brand |

| Customer relationship control | Reduced direct control over payment identity | Higher control than MoR | Highest control | Shared or reduced control |

| Operational burden | Lower internal burden | Moderate burden | Highest burden | Lower to moderate, depending on partner |

| Best fit | Teams prioritizing speed and compliance outsourcing | Teams wanting flexibility without full liability transfer | Companies with internal finance, legal, and payments capability | Businesses that rely on channel distribution or platform sales |

What this means in plain English

If you use Stripe as a PSP, you get payment processing infrastructure, but you still own much of the commercial and regulatory responsibility around the sale.

If you become your own merchant of record, you keep control. You also keep the headaches. That can work for larger SaaS companies with the right finance, tax, and legal muscle. It's a bad idea for teams that are still improvising basic billing operations.

If you sell through a marketplace or reseller, you may offload commercial burdens, but you also lose direct ownership of the customer relationship and brand presentation.

The right model depends less on product category and more on how much liability, control, and complexity your team can absorb without slowing growth.

That's the lens founders should use. Not “Which billing logo do other startups use?” but “Which commercial structure supports our actual go-to-market and retention motion?”

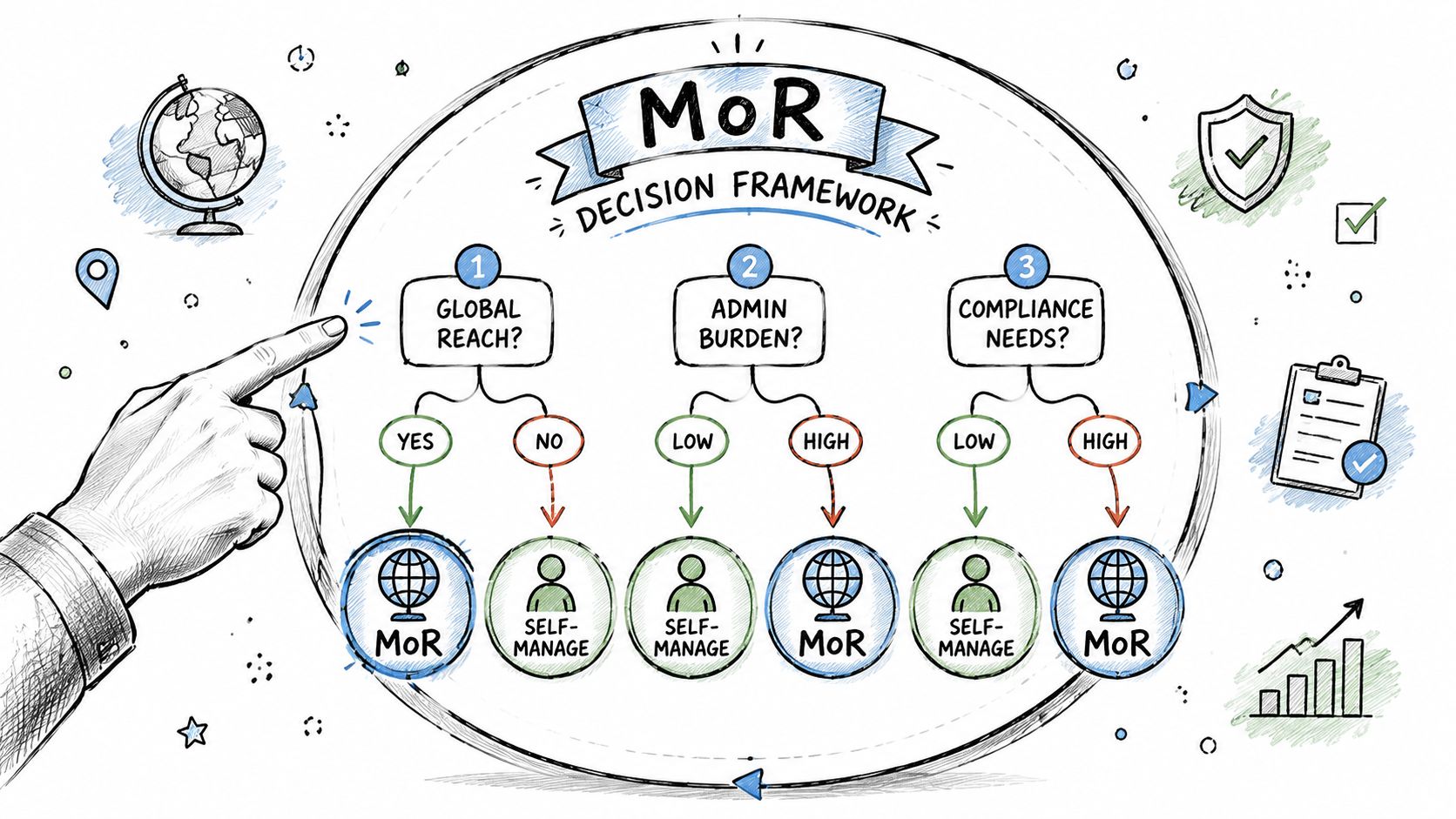

The MoR Decision Framework for Your Business

The wrong way to choose an MoR is to ask whether it makes global selling easier. Of course it does. The right question is whether it makes your business better once acquisition, renewals, cancellations, and recovery are all included.

Ask the finance questions first

Start with the questions most founders delay:

- How much international revenue justifies outsourcing? If global sales are still early and operational capacity is thin, an MoR may be the pragmatic move.

- How sensitive is your margin to discounts and saves? If retention depends on aggressive renewal offers, MoR economics deserve deeper scrutiny.

- Can your team own compliance internally without distraction? If not, outsourcing may still be worth the tradeoff.

These are not abstract finance questions. They determine whether your billing model supports profitable growth or just convenient growth.

Then ask the customer experience questions

Many implementations often go wrong at this stage.

If your buyer is an enterprise admin, procurement lead, or finance approver, trust signals matter. Recent surveys indicate that 28% of enterprise customers hesitate to renew subscriptions when the MoR's name is not aligned with their primary vendor, leading to involuntary churn, according to Numeral's discussion of merchant of record ecommerce issues.

That means statement descriptors, receipt branding, invoice clarity, and support handoff are not cosmetic details. They affect renewal behavior.

You should pressure-test:

- Descriptor clarity: Will customers recognize the charge instantly?

- Receipt consistency: Does the post-purchase trail match your brand?

- Support ownership: When billing confusion happens, who resolves it fast?

Don't ignore downstream workflow friction

If you run Stripe and layer an MoR or MoR-like structure into your payment stack, your cancellation and recovery workflows can get awkward. A simple example: your product team wants to offer a pause, downgrade, or targeted discount when a user tries to cancel. But the billing entity, refund path, or statement identity may now live partly outside the flow you control most directly.

The same issue shows up in auto-renewal notices, cancellation disclosures, and billing consent. If your customer base includes California users, you also need to think through operational alignment with rules around renewals and billing communication. This overview of California automatic renewal law is a useful reminder that billing structure and customer communications can't be treated separately.

If your retention playbook depends on flexible save offers, map the MoR impact before procurement signs the contract.

My decision rule

Use an MoR when compliance burden is the urgent bottleneck and brand control is less critical.

Avoid or tightly scrutinize an MoR when your growth model depends on high-touch renewals, clean enterprise billing identity, and margin-sensitive churn recovery. In that case, the convenience may cost more than it saves.

Conclusion Next Steps for Your Payment Strategy

A merchant of record can be a smart move. It can also be an expensive shortcut.

If your team needs fast international expansion and doesn't want to build tax, compliance, and liability handling in-house, the model solves a real operating problem. That's why it has become common in SaaS. But convenience in the selling layer can create friction in the retention layer, and that's where many founders get surprised.

The two big risks are clear.

First, margin erosion. If your save strategy relies on discounts, percentage-based MoR fees can eat into the economics of churn recovery. Second, brand distance. If customers see a third party instead of your company in the billing trail, trust can weaken at the worst possible time, especially around renewals and failed-payment confusion.

That doesn't mean “don't use an MoR.” It means treat the choice like a revenue design decision, not just a payments implementation.

Three next steps I'd recommend

- Audit your current revenue mix

Break down where your customers are, how much revenue is international, and where billing complexity is creating drag today. - Model the margin impact before signing

Don't stop at top-line fees. Run the MoR economics through discounts, renewal saves, refunds, and failed-payment recovery scenarios. - Review your cancellation and recovery flows

Check whether an MoR will make it harder to run pauses, downgrades, card updates, clear renewal notices, and other save motions that protect recurring revenue.

Founders who do this work early make better tradeoffs. Founders who don't usually find out later, when support volume rises, renewal friction increases, and finance starts asking why “saved” customers aren't producing the margin they expected.

If you run subscription software on Stripe and want tighter control over cancellation saves, payment recovery, and churn visibility, Revcover is worth a look. It helps SaaS teams intercept cancellation intent, test save offers like pauses and downgrades, recover failed payments, and tie those outcomes back to recovered recurring revenue without rebuilding core billing logic.