Accepting ACH Payments for SaaS a Complete Guide

Ayush Soni

Founder, Revcover

On this page

- Why Your SaaS Needs a Smart ACH Strategy

- Where ACH fits best

- Choosing Your ACH Payment Provider

- Third-party provider versus direct integration

- Decision criteria that matter in real life

- What works and what doesn't

- Stripe ACH Setup and Bank Verification

- Start with billing design, not code

- Bank account verification methods compared

- A Stripe implementation pattern that works

- Managing ACH Returns and NACHA Compliance

- The return types that actually matter operationally

- What to do after a return lands

- Optimizing ACH for Recurring Revenue and Churn Reduction

- Dunning for ACH needs a different tone

- Make bank account updates easy

- Reconciliation Reporting and Revenue Recovery

- The reporting stack you need

- Measure recovery, not just failure

Your card volume is rising, finance is asking why payment costs keep climbing, and your customer success team is still cleaning up renewals that failed because the buyer's corporate card changed. That's usually when ACH moves from “nice to have” to “we should've done this earlier.”

For SaaS, accepting ACH payments isn't just a checkout project. It changes margin, billing operations, support workflows, and how you recover revenue when a payment fails days after the invoice looked fine. Teams often underestimate that last part. ACH can be attractive on cost, but it introduces a different failure pattern than cards, and recurring revenue teams need to design for that from day one.

The upside is real. Credit card processing fees for SaaS can range from 2.9% + $0.30 per transaction, while ACH payments are often capped, with providers like Stripe charging a maximum of $5, which makes ACH far more cost-effective for subscriptions over $200 according to Stripe pricing. The catch is that you don't get the same instant clarity you're used to with cards. Returns, verification friction, mandate handling, and retry logic matter much more.

Why Your SaaS Needs a Smart ACH Strategy

A familiar scenario plays out in B2B SaaS. A customer signs the order form, the first invoice goes out, and finance comes back with a simple request: pay by bank instead of card. At that point, ACH stops being a nice-to-have billing option and becomes part of how you close, collect, and retain revenue.

For higher-value subscriptions, ACH usually improves unit economics fast. It also fits how many finance teams already pay vendors. But the core reason to build a strategy around it is operational. ACH has a longer lifecycle than cards. A payment can look fine on day one and still come back days later as a return. If the team only focuses on enabling bank payments in checkout or on an invoice, revenue risk shows up later in dunning, support, and reconciliation.

That lifecycle point matters more than the fee discussion.

A card failure is usually immediate and visible. ACH failures are often delayed, and that changes how RevOps, billing, and finance should respond. If Stripe marks a payment as processing, customer success may assume the invoice is covered. If the debit later returns for insufficient funds, a closed bank account, or an authorization issue, the account can slip into a renewal period with revenue already at risk. Without a plan, teams send the wrong message at the wrong time, grant access too long, or create duplicate outreach from billing and support.

Where ACH fits best

ACH tends to perform best in SaaS motions where the buyer already expects a more deliberate payment process.

- Mid-market and enterprise plans: Procurement, approvals, and AP review are already part of the deal.

- Annual contracts or larger monthly invoices: Bank payments become more attractive as invoice size rises.

- Customers with invoice-based AP workflows: ACH matches how their finance team already processes vendors.

- Accounts with renewal exposure from card expiry: A bank account can reduce one common source of involuntary churn.

The mistake I see most often is treating ACH like a cheaper card. Teams add the payment method, confirm the mandate, and stop there. Then returns start landing a few business days later, invoices flip states in Stripe in ways the GTM team did not expect, and no one owns the recovery playbook. That is how avoidable revenue leakage starts.

Practical rule: Build ACH as an end-to-end revenue collection workflow, with ownership for verification, settlement timing, return handling, customer communication, and recovery.

There is also a policy layer to get right. If your subscriptions auto-renew, the ACH authorization flow should line up with your renewal terms, billing disclosures, and customer consent records. Teams reviewing billing UX should also review California automatic renewal law requirements for subscription communication, especially when legal or procurement is already involved in contract language.

A smart ACH strategy does more than lower payment cost. It gives larger customers a payment method they expect, sets realistic rules for service access while funds are still settling, and prepares your team for the failures and returns that will happen. That is what protects MRR.

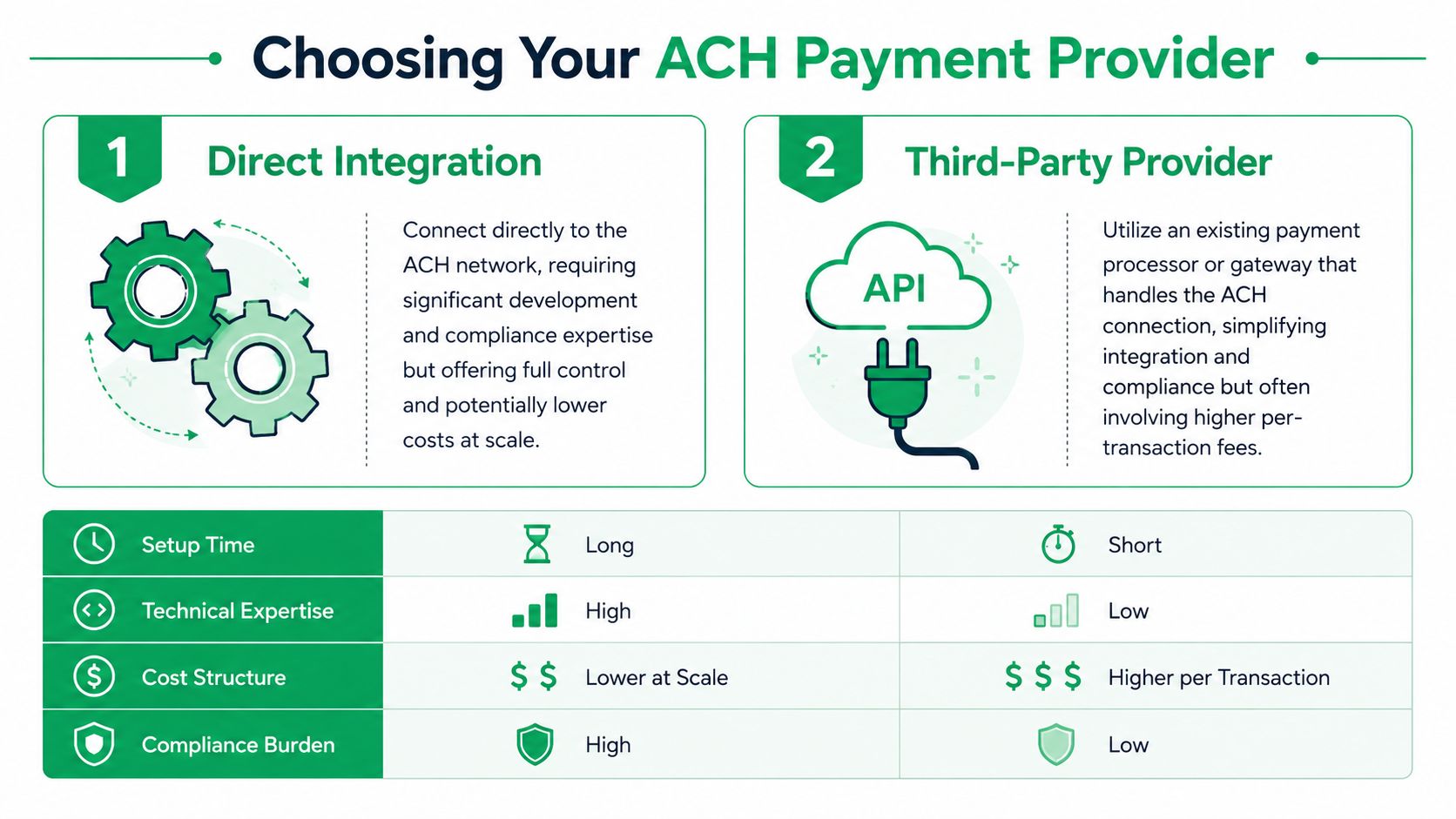

Choosing Your ACH Payment Provider

The provider decision usually comes down to one question. Do you want the fastest path to accepting ACH payments, or do you want the most control over how money movement, risk controls, and billing orchestration work?

Most SaaS companies should start with a third-party processor. The engineering work is lighter, the compliance burden is easier to manage, and the subscription billing stack usually fits your current systems. A direct bank or ACH network approach can make sense later, but it's rarely the first move unless payments are already a core competency inside the company.

Third-party provider versus direct integration

Here's the practical difference.

| Approach | Best fit | Main upside | Main downside |

|---|---|---|---|

| Third-party processor like Stripe | Most SaaS teams | Faster launch and easier integration with billing | Less control over edge cases and fee structure |

| Direct bank or ACH-first setup | Payment-heavy businesses with internal expertise | More control over rails, risk, and ops design | More engineering, more compliance, more maintenance |

A third-party option is usually the better answer when your stack already relies on Stripe Billing, subscription webhooks, revenue tooling, and internal workflows built around one system of record. You don't want payment collection logic fragmented across multiple platforms unless you have a strong reason.

Direct integration changes the shape of the work.

- Engineering gets heavier: Your team owns more of the payment orchestration and bank workflow detail.

- Compliance gets closer: NACHA obligations stop feeling abstract very quickly.

- Support gets more specialized: Returns and mandate questions land in your queue, not just the provider's.

- Finance gets flexibility: If volume is high and process maturity is strong, control can be valuable.

Decision criteria that matter in real life

Founders often overweight transaction fees and underweight operational load. That's backwards in the early stages.

Use this lens instead:

- How quickly do you need ACH live? If the answer is “this quarter,” use a processor.

- Who owns billing engineering? If one product engineer also owns growth experiments, avoid custom rails.

- How custom is your billing model? Usage billing, contract amendments, and hybrid invoice flows can expose limitations sooner.

- How much risk process can finance absorb? ACH returns require discipline even with a provider. Without one, that discipline has to be stronger.

A cheaper payment rail isn't cheaper if your team spends every week reconciling exceptions manually.

What works and what doesn't

What works is choosing the provider that matches your current operating model. For most Stripe-based SaaS companies, that means staying inside Stripe for ACH until volume, complexity, or economics justify something else.

What doesn't work is building a custom payment architecture because one large prospect asked for bank payments. If a single deal requirement drives the roadmap, use the path that gets you live safely and lets you learn from real payment behavior first.

Provider choice should reduce unknowns, not introduce new ones.

Stripe ACH Setup and Bank Verification

Stripe is the common path because it keeps ACH close to the rest of your billing stack. That matters. Your invoices, subscriptions, payment methods, webhook events, and retry logic stay in one ecosystem, which lowers the number of places revenue can get lost.

The friction point is bank verification. That's where many ACH rollouts underperform. The payment method is attractive, but if the buyer hits a confusing bank-linking flow during onboarding, conversion drops before you even create the subscription.

Start with billing design, not code

Before your team enables ACH in Stripe, decide where ACH belongs in the customer journey.

For most SaaS businesses, these patterns work best:

- Offer ACH selectively at first. Start with higher-value plans, annual commitments, or invoice-based accounts.

- Set customer expectations early. Tell buyers they'll verify a bank account and that debit timing differs from cards.

- Separate onboarding from collection when needed. If implementation starts before the first debit clears, align access rules with that risk.

- Store authorization cleanly. Your internal records should make it easy to confirm who authorized bank debits and when.

A poor rollout puts ACH beside card checkout for every account from day one. That sounds flexible, but it can create friction in self-serve flows where speed matters more than payment efficiency.

Bank account verification methods compared

The verification experience determines whether users finish setup confidently or abandon halfway through. Stripe typically supports an instant verification path and a manual micro-deposit path. The right answer depends on deal size, urgency, and customer type.

| Method | User Experience | Verification Speed | Typical Cost | Best For |

|---|---|---|---|---|

| Instant verification | Smooth when customer is comfortable linking bank access in-session | Faster | Provider-dependent | Sales-assisted onboarding, higher-intent buyers |

| Micro-deposits | More steps and delayed completion | Slower | Usually simpler operationally | Buyers who won't use instant verification, fallback flows |

Instant verification usually converts better because it finishes in one session. It also creates a trust hurdle. Some finance teams won't connect credentials through a third-party flow, even if the experience is standard. That's why micro-deposits still matter. They're slower, but they give cautious buyers a fallback instead of a dead end.

If you only support one verification path, make it the one your actual buyers will complete, not the one your team prefers.

A Stripe implementation pattern that works

The cleanest setup is to treat ACH as a saved payment method attached to the customer, then create the subscription only after verification completes or you've deliberately accepted the pending state.

A practical flow looks like this:

// Server-side example using Stripe's Node library

const customer = await stripe.customers.create({

email: 'buyer@example.com',

name: 'Acme Finance Team'

});

const subscription = await stripe.subscriptions.create({

customer: customer.id,

items: [{ price: 'price_recurring_saas_plan' }],

default_payment_method: 'pm_bank_account_id',

payment_behavior: 'default_incomplete',

expand: ['latest_invoice.payment_intent']

});That default_incomplete pattern is useful because it gives you room to complete verification and confirm payment state before treating the subscription as fully healthy.

You also need webhook handling. ACH is not the place for polling and assumptions.

// Minimal webhook sketch

switch (event.type) {

case 'invoice.payment_succeeded':

// provision or continue service

break;

case 'invoice.payment_failed':

// trigger ACH recovery workflow

break;

case 'customer.subscription.updated':

// sync billing state to your app

break;

default:

break;

}A few Stripe-specific pitfalls show up repeatedly:

- Provisioning too early: Don't assume ACH initiation means cleared funds.

- No fallback verification path: Buyers get stuck if instant verification fails and support has no alternative.

- Weak webhook ownership: If billing events aren't reconciled into your app, support sees one state and finance sees another.

- Generic failure messaging: “Payment failed” is too vague for ACH. Customers need next-step guidance.

The strongest implementation is boring in the best way. The buyer understands the flow, finance can trace authorization, engineering trusts webhook-driven state changes, and support knows what to say when bank verification stalls.

Managing ACH Returns and NACHA Compliance

Cards usually fail fast. ACH often fails later. That single difference changes your operating model.

An ACH debit can be initiated, appear normal, and then come back as a return after the customer has already received an invoice receipt or product access. If you don't have a response plan, finance, support, and customer success end up improvising against the same account with conflicting messages.

The return types that actually matter operationally

You don't need everyone on the team memorizing every code. You do need a shared playbook by category.

| Return category | Example codes | What it usually means | Best immediate action |

|---|---|---|---|

| Temporary funds issue | R01 | The account lacked funds at that moment | Retry on a controlled schedule |

| Account data problem | R03 | Account details are invalid or unusable | Stop retries and collect new bank details |

| Authorization issue | Unauthorized-related returns | Customer or bank is challenging the debit authorization | Pause collection and review mandate records |

| Account status issue | Closed or blocked account types | The account can't accept debits | Move customer to a new payment method |

R01 and R03 are the codes most revenue teams should know on sight. R01 means insufficient funds. R03 means no account or unable to locate account. They require different handling. Retrying an R01 can work if customer communication is clear and timing is sensible. Retrying an R03 without collecting corrected details usually just creates more failures.

What to do after a return lands

A workable response flow looks like this:

- Classify the return. Temporary, data issue, authorization issue, or hard stop.

- Freeze automated assumptions. If your app granted access based on initiation alone, review account status.

- Send a customer-specific message. “Please update your bank details” is different from “we'll retry shortly.”

- Create an owner. Finance may reconcile it, but customer success or support may need to save the renewal.

- Document the authorization trail. This matters most when the return raises an unauthorized concern.

Operational cue: Treat unauthorized returns as a process review, not just a payment recovery event.

NACHA compliance becomes practical here. Teams need to keep authorization records, use debit language that matches what the customer agreed to, and avoid sloppy retry behavior. The easiest way to create avoidable risk is to let automated retries run without distinguishing between insufficient funds and invalid account problems.

What doesn't work is a card-style recovery system pasted onto ACH. Cards can often tolerate generic retries and broad failure buckets. ACH needs narrower rules.

A few habits reduce trouble quickly:

- Map return codes to actions: Don't let agents invent the next step.

- Keep customer communication plain: Buyers should know whether they need to act.

- Audit your mandate copy: Billing pages, order forms, and invoice approvals should align.

- Review repeat offenders: If one customer or segment returns frequently, change the setup process.

Returns are part of accepting ACH payments. The risk isn't that they happen. The risk is handling them casually and turning a recoverable billing issue into churn or a compliance problem.

Optimizing ACH for Recurring Revenue and Churn Reduction

Once ACH is live, the work shifts from collection to continuity. During this phase, many teams leave revenue on the table. They treat ACH failures like card declines, send a generic notice, and hope the customer fixes it.

That's not enough. ACH failures usually need more context, more patience, and tighter coordination between billing logic and customer messaging.

Dunning for ACH needs a different tone

A good ACH dunning sequence assumes the customer may still want the product and may not realize the debit failed until after the fact. The message shouldn't read like a fraud alert unless that's the issue.

The strongest pattern is a coordinated sequence:

- First notice: Explain that the bank payment didn't complete and whether you'll retry.

- Follow-up reminder: Ask for action only when action is needed, such as updating account details.

- In-app prompts: Surface the issue where admins already manage billing.

- Escalation path: Route higher-value accounts to success or sales before access is restricted.

The timing matters, but rigid formulas usually fail. Payroll cycles, procurement approvals, and customer billing habits affect whether a retry succeeds. Your retry schedule should reflect actual customer behavior, not a default template copied from card billing.

A lot of teams already understand the mindset from card recovery. The same principle applies here: involuntary churn falls when you combine retries, clear messaging, and a low-friction update path. The operational logic is similar to the retention lessons behind handling issuer-driven payment failures, even though ACH fails for different reasons.

“Your payment failed” is rarely enough information for a finance contact to resolve the issue quickly.

Make bank account updates easy

If the customer needs to switch banks, re-verify an account, or move from ACH to card, the update flow should be obvious and fast.

What works:

- Admin-only billing actions: Let the right account owner fix payment details without opening a support ticket.

- Clear fallback options: If bank verification fails, offer another secure path.

- State-aware product behavior: Don't surprise users with abrupt lockouts when a retry is still in progress.

- Internal visibility: Sales, success, and support should see whether a billing issue is active and what step comes next.

What doesn't work:

- Sending users to Stripe-hosted flows with no context

- Asking support to manually explain return codes

- Hiding payment method updates behind too many clicks

- Restricting product access before your own retry plan finishes

There's also a customer relationship point here. For many B2B accounts, the person who notices a product access issue isn't the person who manages the bank account. Your billing recovery flow should bridge that gap. The in-app notice goes to the admin. The email goes to billing and account contacts where appropriate. The CRM owner sees the account risk before renewal is jeopardized.

Recurring ACH revenue stays healthy when payment recovery feels like part of account management, not a separate collections function.

Reconciliation Reporting and Revenue Recovery

An ACH invoice can look fine on day one and still turn into a revenue problem a few days later. In SaaS, that lag is where weak reporting breaks down. Finance sees a payment attempt, support sees an access complaint, customer success sees renewal risk, and nobody has a shared view of what needs action.

The reporting stack you need

Stripe gives you the raw payment events. It does not give you an operating view of revenue risk unless you add account context, ownership, and recovery status on top.

Start with a dashboard your billing, RevOps, and success teams can use every day. It should answer three practical questions fast: what is still pending, what failed and why, and what action is blocked waiting on your team or the customer.

Track at least these views:

| Report | Why it matters | Team that uses it |

|---|---|---|

| ACH payment status by invoice | Shows which invoices are pending, paid, or returned | Finance |

| Return reason view | Separates retriable failures from account correction problems | Finance and support |

| Open recovery queue | Lists accounts that still need customer or internal action | RevOps and customer success |

| Recovered revenue view | Shows which failed payments later became collected revenue | Finance and leadership |

The key is prioritization. A returned ACH on a low-value monthly account should not sit in the same queue as a failed annual invoice tied to an expansion or renewal. If your team works from a flat failure list, high-risk accounts wait too long.

Measure recovery, not just failure

Teams usually start ACH reporting by counting adoption and lower processing costs. The harder part, and the part that protects MRR, is measuring what happens after the payment fails.

A useful recovery model answers questions like these:

- Which return types tend to recover with retries

- Which return types require a bank account update or a customer contact

- How long it takes from first failure to cash collected

- Which outreach sequence or owner intervention led to resolution

- Whether product access changes helped collection or increased churn risk

That discipline matters outside billing too. If your team already uses a revenue attribution model for growth and retention decisions, apply the same thinking here. Payment recovery should not be a black box labeled "collections." It should be measurable operational work tied to retained revenue.

One habit makes a big difference. Log the action that happened before recovery, not just the final successful payment.

Stripe's event history is helpful, but it is not enough for SaaS revenue operations. You also need to capture who contacted the customer, whether a retry was manual or automated, whether the account changed banks, whether access was limited, and whether the issue was resolved before the next billing cycle. Without that layer, reconciliation stays manual and revenue recovery stays hard to improve.

Good ACH reporting closes two gaps at once. Finance can reconcile cash and open receivables correctly. Revenue teams can see which failed payments are still recoverable before they turn into churn.