Card Declined by Issuer: A SaaS Guide to Revenue Recovery

Ayush Soni

Founder, Revcover

On this page

- Introduction The Silent Churn Driver

- What Card Declined by Issuer Really Means

- The bank makes the decision

- Three practical buckets

- Decoding Stripe Decline Codes and Webhooks

- Why generic messages create bad workflows

- Stripe decline codes and recommended actions

- Use webhooks to trigger recovery

- Building Your Initial Payment Recovery Playbook

- Start with a decision tree

- Write customer messaging that helps

- Operationalize the workflow

- Advanced Recovery Strategies for Subscription Businesses

- Move beyond retries

- Treat access and grace periods as retention levers

- Measuring and Reducing Involuntary Churn

- Track the right operating metrics

- Run experiments that change outcomes

- Conclusion From Reactive Fixes to Proactive Retention

A subscription payment fails at 2:13 a.m. Stripe marks the invoice unpaid. Your product still has active users in the account. Customer success sees nothing yet. Finance sees the miss later. A few days pass, retries fail, access gets restricted, and the customer disappears.

That sequence looks operational. It's a revenue problem.

In SaaS, a card declined by issuer rarely shows up as a dramatic churn event. It arrives as a failed renewal, a vague decline message, and a queue of accounts that “might recover.” Teams often treat those failures as billing noise. That's a mistake. One payments guide says about 5 to 10% of all card transactions are declined on average, depending on industry and transaction type, which is why issuer declines can become a real churn driver for subscription businesses if retries aren't handled intelligently (Clearly Payments on average card decline rates).

The practical takeaway is simple. If you run a recurring revenue business, failed payments deserve the same rigor you apply to acquisition, onboarding, and expansion. The companies that recover more revenue usually aren't doing anything magical. They classify declines correctly, react based on the signal Stripe gives them, and run a measured recovery workflow instead of blasting generic reminders.

Introduction The Silent Churn Driver

The most dangerous churn issues usually don't announce themselves. They hide in routine billing failures that get routed to finance, support, and product in pieces. One team sees an unpaid invoice. Another sees a frustrated customer. Nobody owns the full recovery path.

That's why involuntary churn tends to linger. A customer may still want the product, still need access, and still be willing to pay. But if the issuer blocks the charge and your system responds with clumsy retries or a generic “update your card” email, you lose revenue for avoidable reasons.

I've seen this pattern enough to treat it as a RevOps problem, not a payments edge case. The teams that recover revenue consistently have one habit in common. They don't stop at “payment failed.” They ask what kind of failure it was, what action the customer should take next, and whether the account deserves a softer off-ramp while billing gets fixed.

Practical rule: A failed recurring charge is not a conclusion. It's an event that should trigger classification, customer communication, and a timed recovery sequence.

There's also a mindset shift that matters. Many operators assume issuer declines mainly come from fraud controls. In practice, that's too narrow. If you build your workflow as if every decline is suspicious, you'll overreact, annoy legitimate customers, and cancel subscriptions that were still recoverable.

The better framing is this: card declined by issuer is a business signal with multiple root causes. Some are temporary. Some are permanent. Some require a retry. Others require a card update, a bank call, or a different payment method. Revenue recovery starts when your system can tell the difference.

What Card Declined by Issuer Really Means

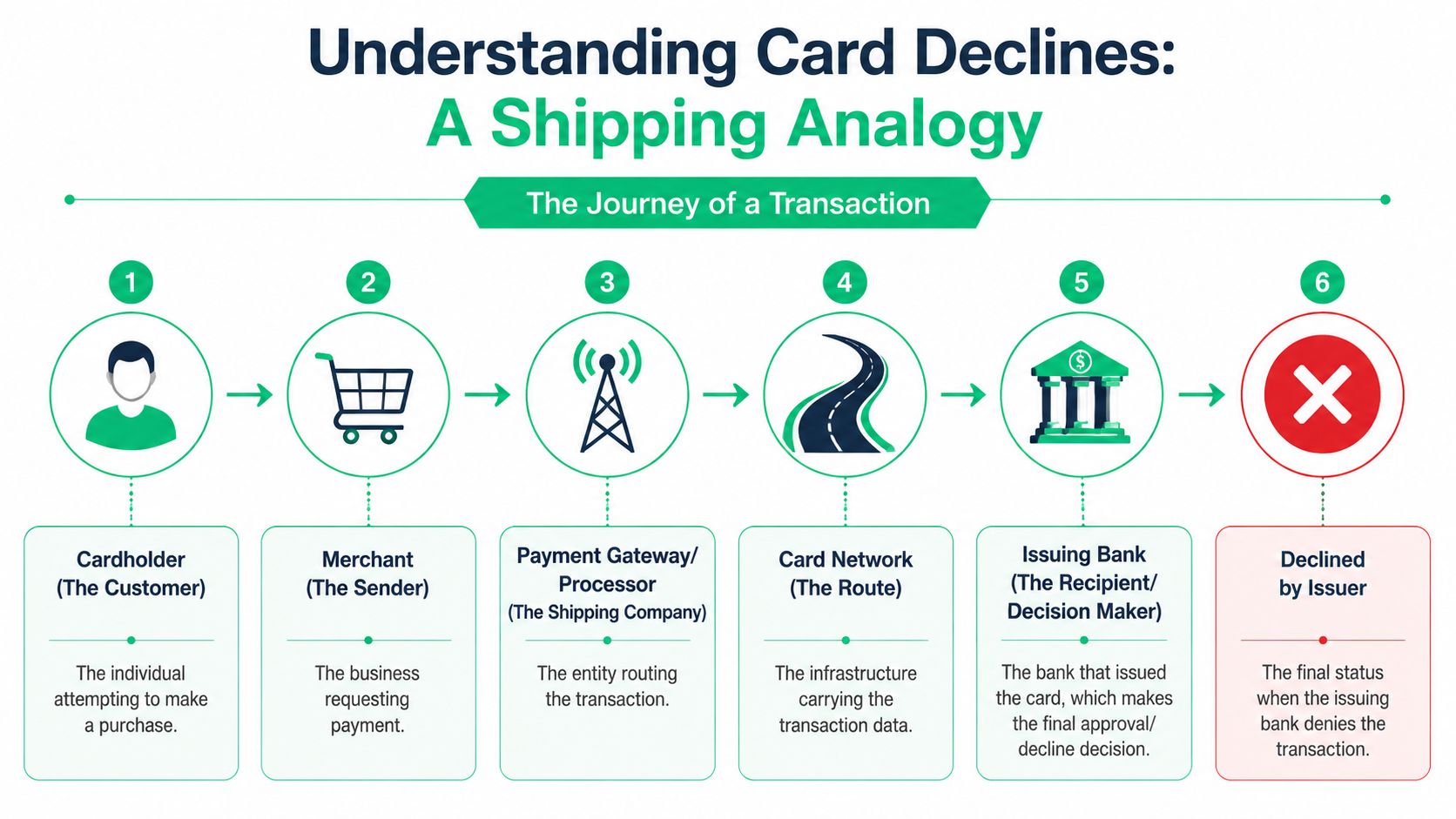

A card transaction passes through several parties, but the final yes or no sits with the bank that issued the card. The merchant requests payment. The processor routes the request. The card network carries it. The issuer decides whether to authorize it.

That distinction matters because teams often debug the wrong layer. They look for a checkout bug, a gateway outage, or a product-side billing issue when the refusal came from the customer's bank.

The bank makes the decision

A simple analogy helps. Think of your billing system as the sender, Stripe as the routing layer, and the issuer as the receiver with the authority to accept or reject the request. If the issuer says no, the merchant doesn't get to override it.

That's why the same surface message can hide very different realities. One industry breakdown estimates that 44.4% of issuer declines are caused by insufficient funds, while 9.4% are tied to fraud suspicion and 10.4% involve cards already reported lost or stolen (myPOS breakdown of issuer decline causes). The biggest bucket in that data isn't fraud. It's funding.

Three practical buckets

For day-to-day operations, I'd simplify issuer declines into three buckets.

- Funding issues. The customer doesn't have enough available funds or credit at the moment of authorization. These cases are often worth retrying with a smart schedule.

- Risk issues. The issuer's fraud controls didn't like the transaction. That doesn't always mean fraud occurred. It means the bank wasn't comfortable approving it without more confidence.

- Card status issues. The card may be expired, replaced, blocked, or no longer valid for the attempted charge. These usually need customer action rather than repeated retries.

Here's the practical point. Your team doesn't need perfect visibility into the issuer's internal logic to improve recovery. It needs a working model for triage.

If the bank refused the payment, your job is to choose the next best action, not to keep sending the same request and hoping the issuer changes its mind.

That's where many billing workflows break. They treat every decline the same. The result is noisy retries on bad payment methods, weak messaging for recoverable accounts, and unnecessary subscription loss.

Decoding Stripe Decline Codes and Webhooks

Stripe gives you much better signals than the customer-facing error message suggests. But many teams never convert those signals into business logic. They store the failure, send a generic email, and leave recovery performance on the table.

Why generic messages create bad workflows

“Do not honor” sounds actionable, but it isn't. It tells you the issuer declined the authorization without giving the merchant a useful plain-English explanation. Stripe's decline code catalog also includes network-level responses like 01 (refer to issuer), 05 (do not honor), and 91 (issuer or switch unavailable), plus recurring-payment stop indicators like R0/R1 when a cardholder has explicitly asked for recurring charges to stop (Stripe decline code reference).

That matters because two failed charges can look identical inside the product while requiring opposite responses:

- A temporary issuer or switch issue may justify another attempt later.

- A cardholder-requested stop on recurring billing should push you toward a card update or alternative payment method, not more retries.

- A fraud-related block may require the customer to contact the issuer directly.

The job isn't to memorize every code. It's to map code families into actions your billing system can execute.

Stripe decline codes and recommended actions

| Stripe Code | Meaning | Decline Type | Recommended Action |

|---|---|---|---|

do_not_honor |

Issuer declined without a specific merchant-facing reason | Review manually | Ask the customer to contact their bank or use another payment method. Avoid aggressive retries. |

insufficient_funds |

Not enough available funds or credit | Soft decline | Retry on a measured schedule and notify the customer with a direct payment update path. |

issuer_not_available or network-level unavailability such as code 91 |

Issuer or switch unavailable | Soft decline | Retry later. Don't escalate to cancellation quickly if the account is otherwise healthy. |

lost_card |

Card reported lost | Hard decline | Stop retries. Prompt for a new card or different payment method. |

stolen_card |

Card reported stolen | Hard decline | Stop retries and request a replacement payment method. |

expired_card |

Card can't be authorized because it's no longer current | Hard decline until updated | Send the customer to update billing details. |

authentication_required |

Additional authentication is needed | Conditional decline | Trigger customer action to complete authentication if your flow supports it. |

card_not_supported |

Card can't be used for this transaction type | Hard or structural decline | Ask for a different card or payment method. |

invalid_account or invalid account number variants |

Payment credentials are not usable | Hard decline | Don't retry. Request corrected payment information. |

R0 or R1 |

Cardholder requested a stop on recurring charges | Hard decline for recurring billing | Pause recurring attempts and route the account to a billing update or retention workflow. |

Use webhooks to trigger recovery

In Stripe environments, the operational center of gravity is the failure event. For many teams, that starts with payment_intent.payment_failed or the related invoice failure signals tied to subscription billing. The exact event names matter less than the discipline around them.

Build your workflow so the webhook does three things immediately:

- Classify the decline into a retryable, customer-action, or stop category.

- Tag the account inside your CRM or customer system so support, success, and RevOps see the same billing state.

- Launch the next touch. That could be a retry timer, an email with a secure card update link, an in-app prompt, or a task for a human follow-up.

The mistake is letting Stripe be your only recovery engine. Stripe tells you what happened. Your business still has to decide what to do with the signal.

Building Your Initial Payment Recovery Playbook

The first version of a strong dunning workflow doesn't need to be fancy. It needs to be disciplined. Most revenue leakage comes from weak branching logic, poor timing, and messages that force the customer to do too much work.

Start with a visible process map that everyone can use.

Start with a decision tree

A good playbook starts with a blunt question: should you retry, or should you stop and ask for a new payment method?

Use logic like this:

- Retry soft declines when the failure looks temporary, such as insufficient funds or issuer unavailability.

- Stop on hard declines when the card is lost, stolen, invalid, unsupported, or blocked for recurring use.

- Escalate customer-action declines when the payment likely needs authentication or direct issuer involvement.

What doesn't work is a fixed retry schedule applied to every failure. That creates noise for banks, confusion for customers, and unnecessary delay for your internal teams.

Operating principle: Retry because the signal says the problem may clear. Don't retry because “that's what the billing system does.”

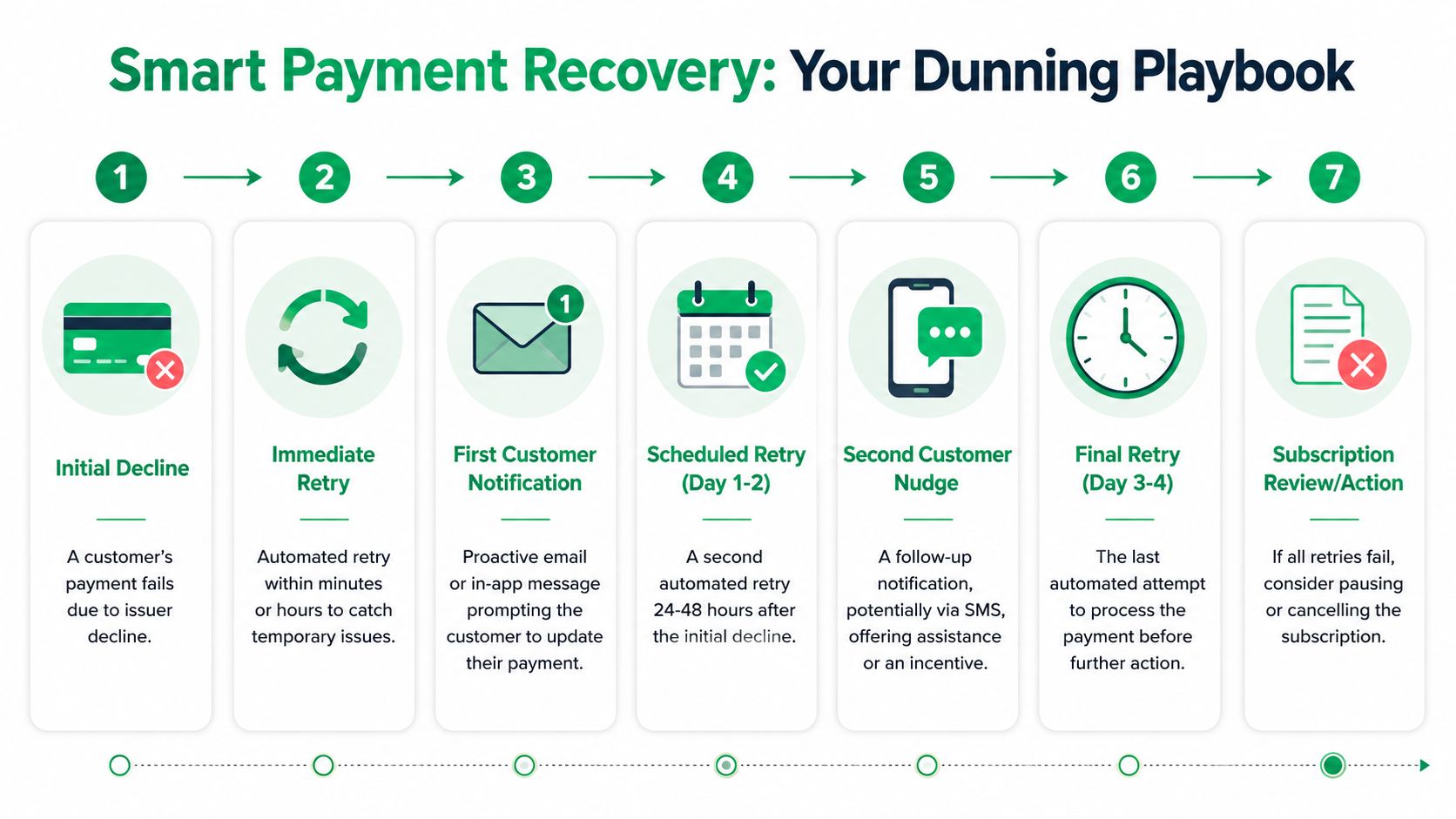

A practical baseline looks like this:

- Immediate short retry for issues that may have been transient.

- Customer notice soon after with a direct, secure route to update payment details.

- Scheduled follow-up retries for retryable declines only.

- Access review before cancellation, especially for active or high-value accounts.

- Stop further attempts when Stripe indicates the payment method won't become valid through timing alone.

For teams that want to centralize this logic with retention workflows, billing context, and product access rules, tools built for subscription recovery can help coordinate that process alongside Stripe Billing, such as Revcover for subscription payment recovery.

A short walkthrough of dunning mechanics can help your team align on the basics:

Write customer messaging that helps

Most failed-payment emails are too vague. “Your payment couldn't be processed” is true, but it doesn't reduce friction.

Your best messages usually include:

- A plain next step. Update your card, try another payment method, or contact your bank.

- A direct path. Don't make the customer hunt through account settings.

- A calm tone. Don't imply fraud or wrongdoing when the issue may just be available funds.

- A clear consequence. Explain whether access will continue temporarily, pause soon, or stop on a specific date.

Avoid stuffing every email with issuer jargon. The customer doesn't need code families. They need clarity.

Operationalize the workflow

Your initial playbook should be visible across teams, not trapped inside Stripe settings.

I'd put ownership on a cross-functional loop:

- RevOps owns routing logic and billing-state definitions.

- Lifecycle or growth owns messaging across email and in-app channels.

- Support owns exception handling when customers reply with issuer-specific problems.

- Product owns grace-period behavior and how account access changes during recovery.

That structure keeps payment recovery from turning into a slow handoff between finance and support.

Advanced Recovery Strategies for Subscription Businesses

Once your basic workflow is in place, the next gains usually come from orchestration. Retries alone won't recover every account worth saving. The better systems combine payment operations, customer communication, and product experience.

Move beyond retries

A mature recovery flow treats the failed charge as one signal among several. You should also ask:

- Is the user still active in the product?

- Is the account high-value enough to deserve more personalized handling?

- Is the decline type pointing to card replacement rather than delayed funds?

- Has the customer already seen prior reminders and ignored them?

Those inputs let you choose the right channel and level of urgency. An active admin logging in every day shouldn't get the same treatment as a dormant self-serve account. For the active account, an in-app billing prompt often outperforms another generic inbox reminder because it appears where the customer is already engaged.

The strongest recovery programs also reduce the number of declines that require customer work in the first place. If your billing stack supports card detail refresh or account update services, use them. If your messaging tools support deep links into a hosted billing portal or secure update flow, use those too. Every extra click lowers the chance of recovery.

Good recovery systems remove effort. Bad ones send reminders that ask the customer to solve the whole problem alone.

Treat access and grace periods as retention levers

Immediate cancellation is usually the laziest response to a failed renewal. It may protect policy consistency, but it often hurts revenue and customer experience.

A better approach is to define grace-period rules intentionally:

- Full access for a short window when the decline looks temporary and the account is healthy.

- Limited feature access when payment remains unresolved but you want to preserve urgency without burning goodwill.

- Pause or cancellation only after your recovery sequence and customer communication have had a fair chance to work.

Product and RevOps need to align. If product shuts the account too early, lifecycle messaging can't do its job. If you leave access open too long with no friction, customers learn they can ignore billing prompts.

The trade-off is real. Strong retention systems are firm about billing, but they're not clumsy about it.

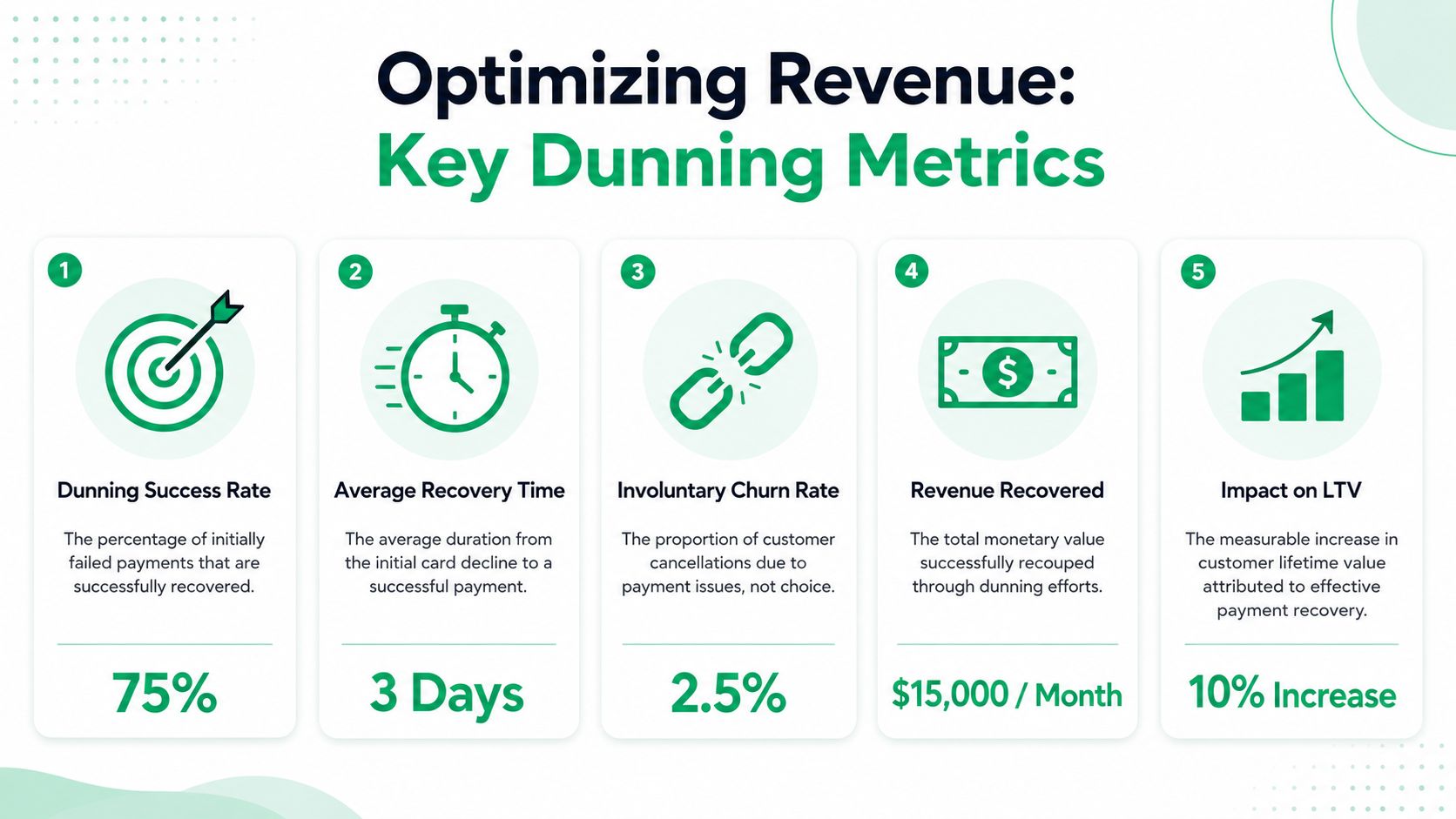

Measuring and Reducing Involuntary Churn

If you don't measure payment recovery as an operating system, you'll end up treating every billing fix as anecdotal. That's how teams keep the same weak sequence for months.

Track the right operating metrics

You don't need exotic analytics. You need a small set of metrics with clear owners.

- Payment recovery rate. Of all failed recurring payments, how many return to paid status during your recovery window?

- Involuntary churn rate. How many customers are lost because billing failed rather than because they chose to cancel?

- Time to recovery. How long does it usually take from first decline to successful payment?

- Touchpoint effectiveness. Which email, in-app message, or retry event tends to precede successful recovery?

- Decline mix by category. Are you mostly dealing with temporary funding issues, card status problems, or recurring stop requests?

Those metrics tell you where to intervene. If recovery happens mostly after the first in-app prompt, invest there. If accounts with hard declines keep receiving retries, fix your branching logic.

Run experiments that change outcomes

Payment recovery should be tested like a growth funnel. The point isn't to add more touches. It's to improve the right ones.

Here are experiments worth running:

- Timing tests. Compare an earlier customer reminder against a later one for soft declines.

- Channel tests. Test email alone versus email plus in-app notification for active users.

- Copy tests. Compare a neutral billing reminder against one that stresses continuity of access.

- Landing-path tests. Reduce steps between the message and the billing update screen.

- Grace-period tests. Evaluate whether a short full-access period or an earlier feature restriction recovers more accounts without increasing abuse.

Measurement lens: Don't judge a dunning sequence by open rates alone. Judge it by recovered subscriptions and prevented involuntary churn.

The useful discipline here is attribution. Tie recovery back to the workflow step that likely drove it. Otherwise your team will optimize for activity, not outcomes.

Conclusion From Reactive Fixes to Proactive Retention

A card declined by issuer isn't just a payment error. It's a decision from the customer's bank that creates a retention moment for your business. Teams that treat it as a technical nuisance usually accept more churn than they need to. Teams that treat it as a revenue workflow recover more subscriptions with less friction.

The pattern is consistent. Read the Stripe signals correctly. Separate retryable declines from dead ends. Contact customers with clear next steps. Give active accounts a measured path to stay live while billing gets fixed. Then track recovery like a growth function, not a support side task.

When you do that well, failed payments stop being a silent leak in MRR. They become one more lifecycle system you can improve.

If you want a tighter way to manage failed payments, cancellation intent, and recovered MRR in one Stripe-connected workflow, Revcover gives subscription teams a practical system for payment recovery, save offers, and retention reporting without rebuilding core billing logic.