Deferred Revenue Definition: A SaaS Guide for 2026

Ayush Soni

Founder, Revcover

On this page

- Introduction The Good Problem You Might Not Understand

- Why this matters outside finance

- Why the number matters in SaaS

- What Is Deferred Revenue A Core Concept Explained

- Why it shows up as a liability

- The Accounting Side Recognition ASC 606 and Journal Entries

- What ASC 606 changed for SaaS teams

- The journal entries in a SaaS subscription

- What product managers should notice in this flow

- Deferred Revenue vs Related Financial Metrics

- Where teams usually get confused

- A quick comparison table

- The Operational Impact of Deferred Revenue on Your SaaS

- Why finance sees a liability and operators should see risk

- Payment failure creates a hidden operational gap

- How RevOps and Product Can Protect At-Risk Deferred Revenue

- What RevOps should own

- What Product should own

- Frequently Asked Questions About Deferred Revenue

- How are upgrades and downgrades handled mid-cycle

- Is deferred revenue the same as a contract liability

- Is deferred revenue always a good sign

- What should a product manager actually monitor

- Why does deferred revenue matter for forecasting

Cash is up. The dashboard looks healthy. Finance closes the month and tells you revenue is lower than the cash that just landed in the bank.

That disconnect catches a lot of SaaS teams the first time they move upmarket or shift from monthly billing to annual contracts. Sales celebrates a prepaid annual deal. The founder sees a bigger cash balance. Then accounting recognizes only a slice of that contract this month, not the full payment.

That gap is where deferred revenue lives.

If you're a product manager, this matters more than it first appears. Deferred revenue isn't just an accounting line item for the controller and auditors. It's a running record of customer commitments you still have to earn through product delivery, retention, onboarding, support, and billing reliability. In SaaS, it can be a large part of the balance sheet. For pre-IPO cloud companies, the average deferred revenue-to-revenue ratio stabilized at 1.35x in 2022, which implies about $1.35 in unearned prepaid cash for every $1 of recognized revenue (SaaS deferred revenue benchmark summary).

That means a meaningful share of your future revenue has already been sold, collected, and promised. It also means some of it is at risk if users fail to adopt, ask to cancel, or hit payment problems before that value is fully delivered.

Introduction The Good Problem You Might Not Understand

A common SaaS moment looks like this. You close a cluster of annual contracts at the end of the quarter, cash jumps, and the team relaxes for a day. Then the monthly financials arrive, and someone asks why recognized revenue barely moved compared with cash collected.

Nothing is broken. The company hasn't earned all of that cash yet.

That prepaid cash becomes deferred revenue because the business still owes service over time. If you sell software access, onboarding, support, or usage rights across a subscription term, you don't earn the whole contract on day one. You earn it as the customer receives the service you promised.

Deferred revenue is one of the cleanest examples of why cash and revenue aren't the same thing.

For SaaS operators, this creates a useful tension. Large prepaid balances usually signal customer commitment and strong collections. But they also represent future obligations. If the product underdelivers, onboarding stalls, renewal intent drops, or billing breaks, the company hasn't just lost a customer. It has disrupted the path by which deferred revenue turns into earned revenue.

Why this matters outside finance

Product managers often look at activation, engagement, expansion, and churn. Finance looks at liabilities, performance obligations, and revenue recognition. Deferred revenue sits right between those worlds.

A customer prepays because they expect value over time. The balance sheet records that promise. The product either fulfills it or puts it at risk.

Why the number matters in SaaS

In subscription businesses, this isn't a niche metric. In the global SaaS market, the average deferred revenue-to-revenue ratio for pre-IPO cloud companies stabilized at 1.35x in 2022, meaning companies held about $1.35 in unearned prepaid cash for every $1 of recognized revenue. That pattern reflects the move toward annual contracts and makes deferred revenue a major operating signal, not just an accounting artifact.

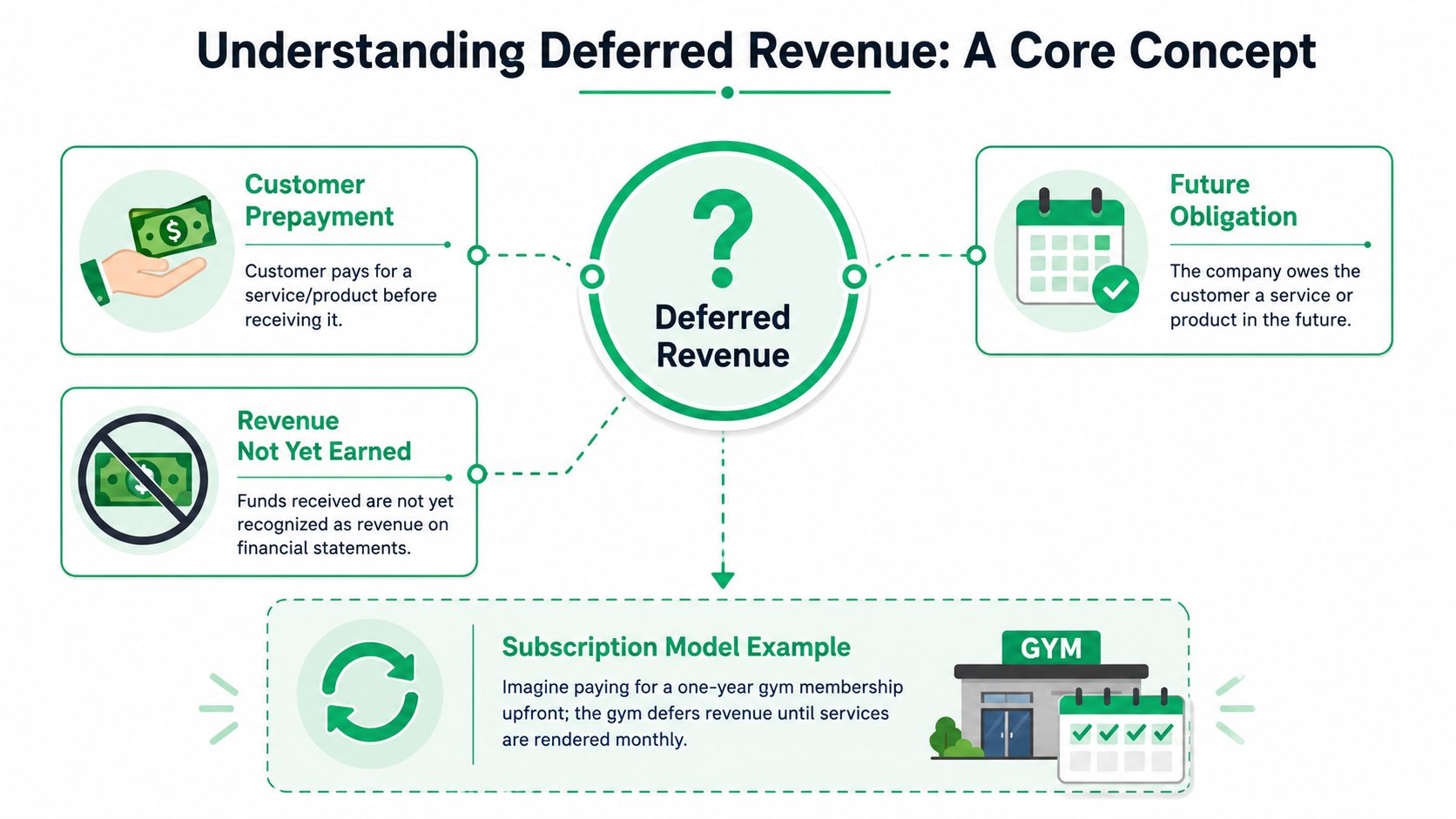

What Is Deferred Revenue A Core Concept Explained

When a SaaS customer prepays for a year of access, the cash arrives immediately, but the service is delivered over the contract period. Until that service is delivered, the payment is not fully earned.

That is the practical deferred revenue definition: cash collected for goods or services the company still owes.

Core definition: Deferred revenue is a contractual liability created when a customer pays in advance and the company still owes future delivery.

In SaaS, that future delivery usually means ongoing access to the product, support, uptime, onboarding, or other contracted services across the subscription term. Finance records the prepayment as deferred revenue because the company has the cash, but it has not yet completed the work tied to that contract.

“Unearned revenue” and “deferred revenue” are often used interchangeably. In practice, both describe the same situation. The customer has paid. The business still has to deliver.

Why it shows up as a liability

The word “liability” causes confusion for non-finance teams because it sounds like debt or a problem. In this case, it means the company owes performance. You have already collected the money, so now the balance sheet reflects an obligation to provide the service promised in the contract.

That accounting treatment matters operationally.

A deferred revenue balance is not just a finance entry waiting to roll into recognized revenue. It is a pool of customer commitment that can still be damaged by failed onboarding, low adoption, preventable cancellations, payment issues, or service interruptions. If a customer prepays in January and churns in March, finance will handle the accounting outcome, but RevOps and Product should care much earlier because the path from cash collected to revenue earned has weakened.

A simple way to read the number is this:

- Cash is already in the business. Collections happened.

- The delivery obligation is still open. Access and service are owed over time.

- Recognition depends on execution. The product experience, billing reliability, and retention motion all affect whether that prepaid value converts cleanly into earned revenue.

For a product manager, this makes deferred revenue more than a technical accounting term. It is a live record of how much value customers have already bet on you delivering. The larger that balance, the larger the amount of prepaid trust sitting on the balance sheet.

The Accounting Side Recognition ASC 606 and Journal Entries

Finance teams don't record deferred revenue just to satisfy auditors. They do it because the timing of revenue matters if you want financial statements to reflect what the business has delivered.

What ASC 606 changed for SaaS teams

The formal standard behind this is ASC 606, issued by FASB in May 2014 and effective for public companies in January 2018. It made deferred revenue treatment more explicit by requiring advance payments to be recorded as a liability until performance obligations are satisfied.

That change had visible effects. In the first year of full compliance, the aggregate deferred revenue liability for the software sector increased by approximately 12.4%, reflecting more conservative and standardized recognition timing.

The practical shift was straightforward. Companies could no longer blur the line between cash receipt and earned revenue. They had to map contract value to actual performance obligations and recognize revenue as those obligations were fulfilled.

Practical rule: If the customer has paid but you still owe service, the amount belongs in deferred revenue, not earned revenue.

The journal entries in a SaaS subscription

Take a simple annual SaaS contract. A customer pays $1,200 upfront for 12 months of access. If the service is delivered evenly across the year, a common treatment is straight-line recognition of $100 monthly.

When the cash is received:

| Account | Debit | Credit |

|---|---|---|

| Cash | $1,200 | |

| Deferred Revenue | $1,200 |

At that moment, the company has cash, but it also has a liability because it still owes product access.

At the end of the first month, after one month of service has been delivered:

| Account | Debit | Credit |

|---|---|---|

| Deferred Revenue | $100 | |

| Revenue | $100 |

That second entry keeps repeating over the contract term as the obligation is satisfied.

What product managers should notice in this flow

Three operational facts sit inside those journal entries.

- Billing starts the accounting trail. The instant the customer prepays, finance records a liability.

- Service delivery enables recognition. Product access, implementation, support, or usage fulfillment is what allows revenue to move out of deferred revenue.

- Interruptions matter. If access is paused, the customer cancels, or service delivery changes mid-contract, finance may need to adjust the recognition pattern.

This is why product changes can affect finance outcomes even when no one changes pricing. If onboarding improves and customers activate faster, the company is more likely to deliver against what it already collected. If customers go dark after purchase, the deferred revenue balance still exists, but the business is carrying a bigger fulfillment and retention burden.

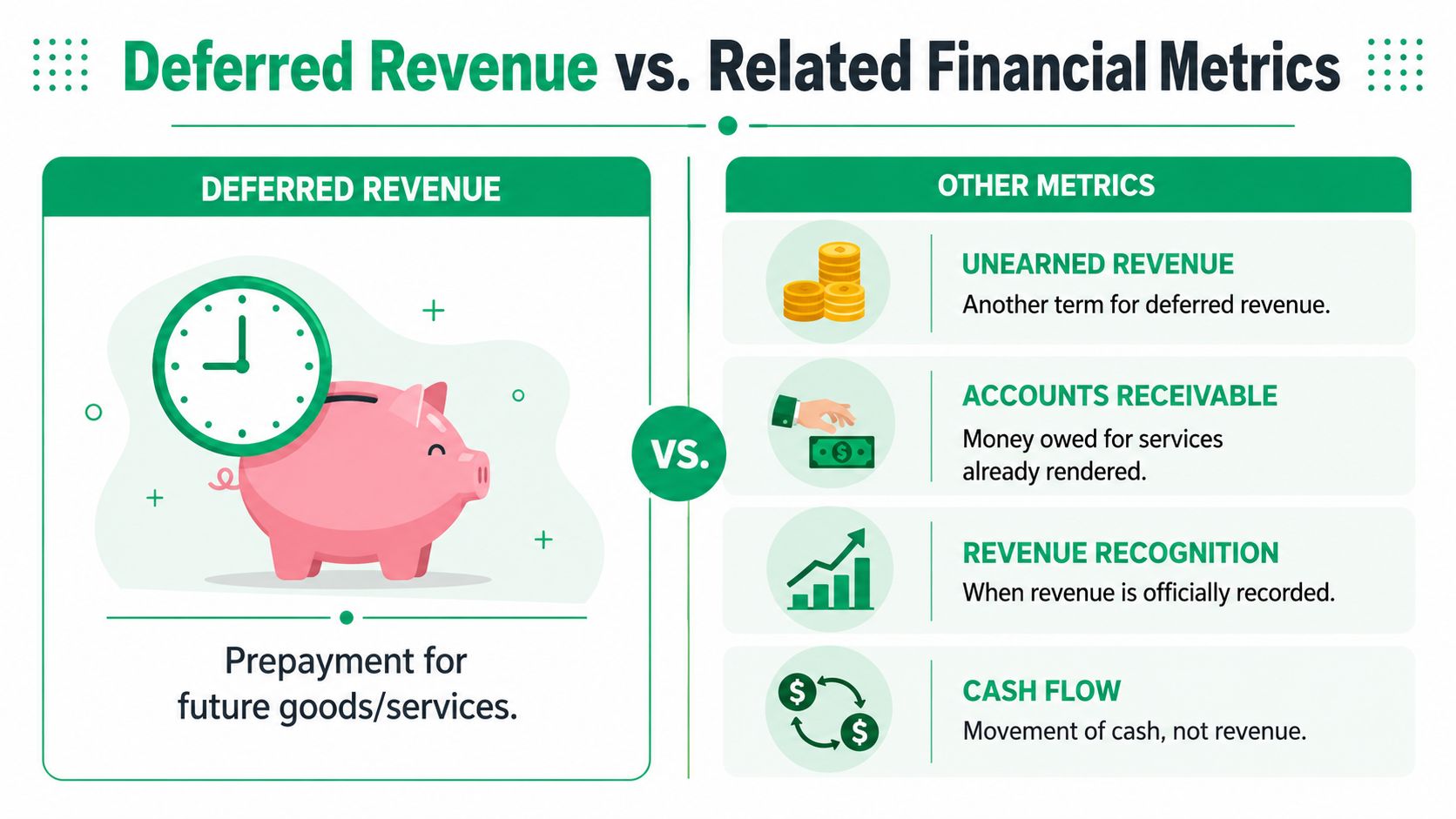

Deferred Revenue vs Related Financial Metrics

Teams usually don't struggle with the deferred revenue definition itself. They struggle with the nearby terms.

Where teams usually get confused

The first confusion is deferred revenue vs unearned revenue. In most SaaS conversations, they're effectively the same thing. Both refer to advance payments for future delivery.

The second is deferred revenue vs accounts receivable. These are opposites in an important way. Deferred revenue means the company has cash before delivery. Accounts receivable means the company has delivered before receiving cash.

The third, and the most common in growth teams, is deferred revenue vs MRR. MRR is a normalized operating metric. Deferred revenue is a balance sheet liability tied to cash already collected.

If you're analyzing retention and expansion, that distinction matters. MRR tells you how recurring revenue is trending. Deferred revenue tells you how much prepaid obligation the company is still carrying. They connect, but they aren't substitutes. This is one reason strong operators pair balance sheet thinking with retention analysis like net dollar retention in SaaS.

A quick comparison table

| Metric | What it represents | Typical balance sheet treatment | Practical SaaS meaning |

|---|---|---|---|

| Deferred revenue | Cash received before delivery | Liability | Customer prepaid, service still owed |

| Unearned revenue | Another term for deferred revenue | Liability | Same concept in most operating discussions |

| Accounts receivable | Cash owed after delivery | Asset | You delivered, customer hasn't paid yet |

| Revenue | Value already earned | Income statement | Delivery obligation satisfied |

| MRR | Normalized recurring revenue view | Not a GAAP balance sheet line | Operating metric for tracking subscription performance |

The fastest way to confuse a planning meeting is to use MRR, cash collections, and deferred revenue as if they describe the same thing. They don't.

A product manager doesn't need to post journal entries, but they do need to know which number answers which question. “Did the customer commit?” is different from “Did we collect?” and both are different from “Did we earn it?”

The Operational Impact of Deferred Revenue on Your SaaS

Once you stop viewing deferred revenue as a static accounting balance, it becomes much more useful. It's a pool of future revenue that the company has already sold but still has to protect.

Why finance sees a liability and operators should see risk

A prepaid customer isn't fully safe just because cash already arrived. The company still has to deliver enough value across the contract term for that commitment to hold up operationally and commercially.

That changes how RevOps and Product should read the balance:

- High deferred revenue can reflect strong customer commitment. Annual prepayment usually means a customer was willing to commit ahead of consumption.

- High deferred revenue also raises the cost of poor execution. If onboarding is weak, support is slow, or usage stalls, you've already collected money against value you still have to prove.

- Cancellation flows matter before renewal. A customer who wants out early may expose product mismatch, budget pressure, or avoidable friction that sits underneath recognized revenue trends.

A useful mental model is this: deferred revenue is future revenue with conditions attached. The condition is that your company keeps delivering what the customer paid for.

Payment failure creates a hidden operational gap

This gets more interesting with involuntary churn. In 2025, Stripe's global failed payment rate hit 14.2% for SaaS subscriptions, which makes payment failure a real operational issue, not just a billing nuisance (Stripe on deferred revenue and advance payment treatment).

When payment issues interrupt service, teams can end up in a messy state. The customer relationship hasn't cleanly ended, but the fulfillment path is no longer smooth. Some operators think of this as an inverted deferred revenue problem. The contract logic, service access, and payment status drift out of sync.

In practice, this shows up when:

- A renewal or installment fails.

- Access is limited or paused.

- The customer updates the card later.

- Teams struggle to determine what was owed, what was delivered, and what should now convert into earned revenue.

That gap isn't just financial. It's product and lifecycle design. Poor retry timing, confusing billing notices, and abrupt access cuts all increase the chance that a recoverable account becomes lost churn. Teams working on payment friction often analyze patterns such as card declined by issuer in subscription billing because the decline reason often tells you whether messaging, retry logic, or customer action should come first.

A failed payment doesn't always mean a lost customer. It often means your systems need to guide the customer back into an active service state before value delivery breaks.

For product managers, this is the operational read-through. Deferred revenue becomes safer when billing continuity, access rules, and recovery communication work together. It becomes riskier when those workflows live in separate tools and separate teams.

How RevOps and Product Can Protect At-Risk Deferred Revenue

The companies that manage deferred revenue well don't leave it entirely to accounting. Finance records it correctly, but RevOps and Product reduce the odds that it turns into leakage.

What RevOps should own

RevOps has the best view of billing events, customer lifecycle stages, and recovery workflows. That puts RevOps in charge of protecting deferred revenue from preventable failure.

A strong RevOps approach usually includes:

- Smarter dunning sequences: Use coordinated retries, clear payment reminders, and direct card-update paths. Generic “payment failed” emails sent on a fixed delay tend to underperform because they ignore billing state and customer context.

- Cancellation routing: Not every cancellation intent should follow the same path. High-value accounts, customers with recent support issues, and users with low product adoption need different handling.

- Clean system handoffs: Stripe, CRM, support tools, and product events need to agree on the account state. If billing says delinquent while product still shows active, reporting gets muddy and recovery teams react too late.

- Reason capture with revenue context: Churn reasons become much more useful when tied to contract value, plan type, and recent billing events.

Teams that separate these streams often miss patterns that sit between voluntary and involuntary churn. That's why many operators look at voluntary vs involuntary churn in subscription businesses as a combined operating problem rather than two unrelated metrics.

What Product should own

Product teams influence deferred revenue more than most dashboards show. They shape whether the promised value is experienced early enough and consistently enough for the contract to hold.

The most effective product habits are operational, not theoretical:

Fix the first-value gap

If customers prepay annually but don't reach value quickly, the deferred revenue balance may look healthy while customer sentiment deteriorates. Onboarding, setup guides, templates, and activation prompts all reduce that gap.

Design cancellation flows for truth, not friction

A cancellation flow shouldn't trap users. It should surface the actual reason for intent and present honest alternatives where appropriate, such as pause, downgrade, or a support conversation. That gives the company a chance to preserve the relationship without hiding the exit.

Treat service interruptions as product moments

Payment recovery isn't only a finance workflow. The in-app experience matters. If a customer sees a dead end, confusing lockout, or no clear update path, the account is harder to recover. If the product clearly explains status and next steps, recovery improves.

Feed finance and success with product signals

Usage drops, repeated setup failures, and unresolved support loops are early warnings that the company is carrying prepaid value at risk. Product teams should push those signals into the same operating conversations where billing and retention are discussed.

The healthiest deferred revenue balance is backed by customers who are actively getting value, not just customers who paid upfront.

This is the trade-off many teams miss. Annual billing improves cash position and visibility. But if the product experience doesn't support sustained value, the company collects risk earlier.

Frequently Asked Questions About Deferred Revenue

How are upgrades and downgrades handled mid-cycle

They usually require the contract to be reassessed and the remaining transaction value to be allocated based on what the customer will receive going forward. In practice, finance needs to reflect the new service level, and product or billing operations need clear rules for access, proration, and effective dates. Otherwise, sloppy plan logic creates downstream accounting cleanup.

Is deferred revenue the same as a contract liability

Deferred revenue is commonly used as the operating term, while contract liability is the formal accounting concept under current standards. In many SaaS situations, the deferred revenue balance is the contract liability tied to advance payment for future service. The key point is still the same: the company owes delivery.

Is deferred revenue always a good sign

Not always. It often signals strong collections and customer commitment, especially with annual billing. But it can also hide execution risk if onboarding is weak, support quality drops, or customers are likely to churn before the contract naturally runs its course. A large balance only helps if the business can convert it into earned revenue cleanly.

What should a product manager actually monitor

Monitor the moments that determine whether prepaid value gets delivered: activation speed, usage consistency, billing friction, cancellation reasons, save offer acceptance, and service interruptions. Finance owns the accounting treatment. Product influences whether that liability keeps moving toward earned revenue.

Why does deferred revenue matter for forecasting

Because it gives the company visibility into revenue that is expected to be recognized in future periods, assuming obligations continue to be satisfied. It doesn't replace retention forecasting, but it sharpens it. A deferred balance backed by healthy usage and low friction is far more reliable than one backed by silent accounts and recurring payment issues.

If your team wants a better handle on the revenue that's already been sold but is still at risk, Revcover helps subscription businesses manage cancellation flows, recover failed payments, and connect those outcomes back to retained and recovered MRR. It works alongside Stripe, gives teams a clearer view of why customers leave, and makes it easier to protect the value sitting behind deferred revenue.