Mastering the Calculation of ARR for SaaS in 2026

Ayush Soni

Founder, Revcover

On this page

- What Is ARR and Why Does It Matter

- The Foundational ARR Calculation From MRR

- Building Your ARR Waterfall From Start to Finish

- The components that actually move ARR

- Sample ARR waterfall structure

- How to Account for Churn and Recovered Revenue

- Not all churn should be treated the same way

- Where recovered ARR belongs in the waterfall

- Handling Advanced Scenarios and Reporting Caveats

- Set rules before edge cases show up

- Usage-based models need a normalization rule

- Keep reporting layers separate

- Common ARR Calculation Mistakes to Avoid

- The mistakes that distort decision making

- The policy test

You're probably in one of two situations right now. Either the board wants a clean ARR number for the next update, or your growth team is debating whether recent saves, downgrades, and failed-payment recoveries should change the headline revenue story.

That tension is normal. The calculation of ARR looks simple until the business starts behaving like a real subscription company. Customers upgrade mid-cycle. Others ask for a downgrade instead of cancelling. Some churn because the product isn't a fit. Others only look churned because a card failed and billing recovery didn't happen fast enough. If you don't separate those motions clearly, ARR becomes less useful precisely when leadership needs it most.

For a Head of Growth, ARR isn't just a finance metric. It's the operating scoreboard that tells you whether acquisition is outpacing leakage, whether expansion is masking underlying retention issues, and whether recovery efforts are preserving revenue that would otherwise disappear.

What Is ARR and Why Does It Matter

Annual Recurring Revenue, or ARR, is the annualized value of recurring subscription revenue. In practice, it answers a simple operating question: how much predictable subscription revenue is the business carrying on a yearly basis right now?

That “predictable” part matters more than is commonly recognized. ARR is supposed to represent durable subscription revenue, not every dollar that happened to land in the bank. One-time services, setup work, pilots, and non-recurring licenses don't belong in the number when you're doing the calculation of ARR for SaaS reporting.

A clean ARR number changes how leaders make decisions. Finance uses it to forecast. Growth uses it to understand whether new logo wins are translating into durable revenue. Product and customer success use it to judge whether retention work is improving the quality of the base, not just adding activity.

Practical rule: If a revenue line won't predictably recur as part of the subscription, keep it out of ARR.

The other reason ARR matters is that it forces discipline across functions. A board deck might show a single headline figure, but that figure is really the output of dozens of operational choices. Did a downgrade reduce recurring value? Did a cancellation get reversed? Did a failed payment recover before the subscription lapsed? Those aren't accounting footnotes. They shape how you interpret growth.

For Heads of Growth, ARR assumes operational usefulness, rather than remaining ceremonial. If your acquisition engine is strong but your cancellation and billing recovery motions are weak, gross new ARR can look healthy while net movement tells a different story. That's why mature teams stop treating ARR as a static snapshot and start treating it as a controlled revenue system.

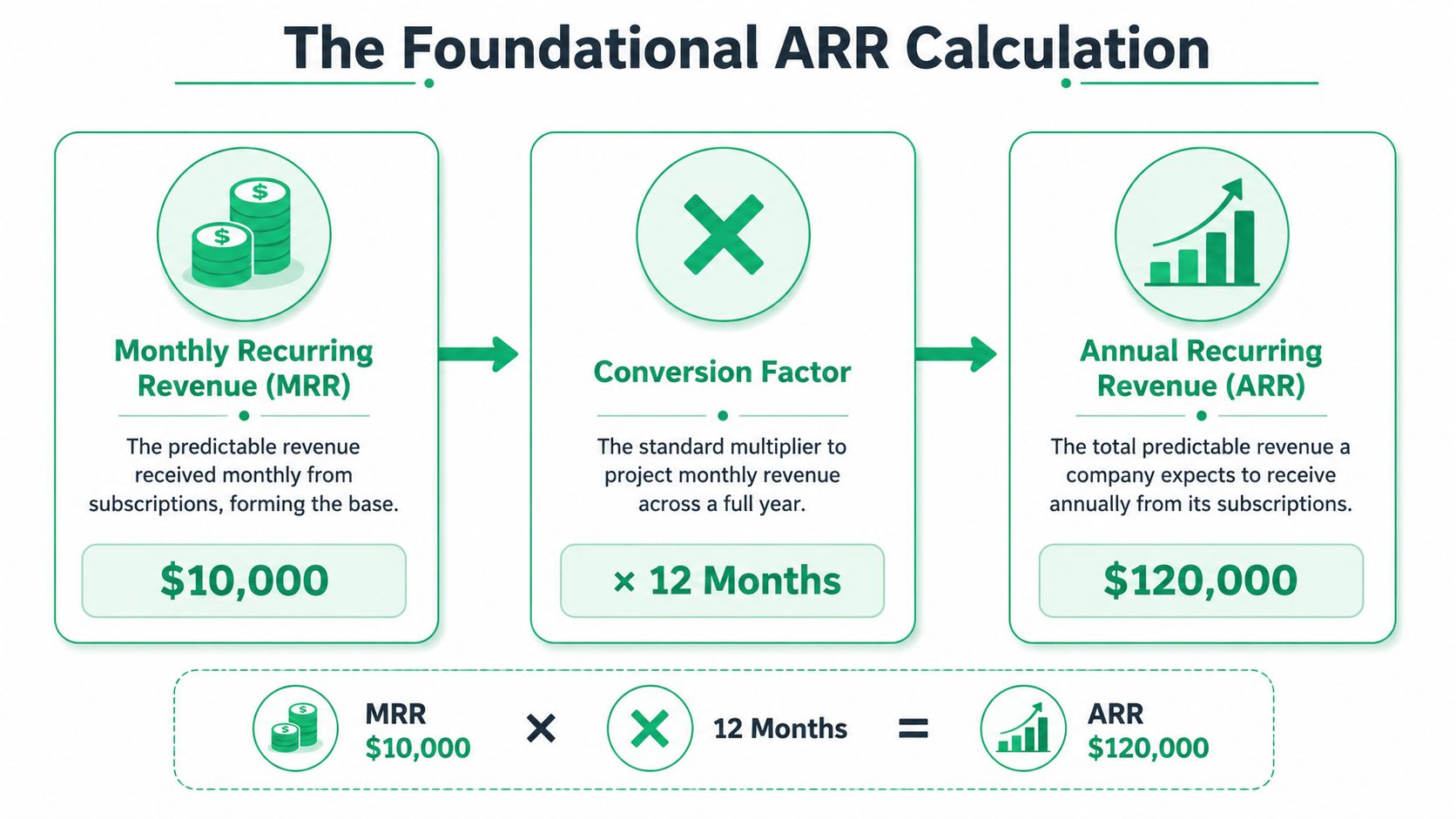

The Foundational ARR Calculation From MRR

A Head of Growth pulls a dashboard before the board meeting and sees MRR up, cash up, and bookings up. Then Finance asks a harder question. How much of that revenue belongs in ARR? That is where the basic formula matters, because clean inputs determine whether ARR is useful or misleading.

The starting calculation is simple. ARR = MRR × 12.

What makes it hard in practice is not the math. It is defining MRR correctly before you annualize it. ARR should reflect recurring subscription revenue at the current run rate. It should not absorb implementation fees, one-off service work, or temporary billing noise just because those amounts showed up on an invoice.

If your company has $100,000 in MRR, ARR is $1,200,000.

That sounds straightforward. Teams still get it wrong all the time because they start from billing exports instead of a recurring revenue policy. Billing systems are built to collect money. ARR reporting is built to measure durable revenue.

Use a simple screening rule before multiplying anything by 12:

- Include recurring subscription charges: Monthly and annual software fees tied to an ongoing subscription belong in ARR.

- Exclude one-time revenue: Setup fees, migrations, implementation, training, and ad hoc services stay out.

- Review pilots and temporary discounts carefully: If the amount does not represent the steady recurring value of the account, do not treat it as ARR.

- Apply one policy across teams: Finance, RevOps, and billing operations need the same inclusion rules or your ARR will shift based on who pulled the report.

Keep ARR separate from accounting balances. If your team also tracks deferred revenue, use a clear definition of deferred revenue in subscription businesses so prepaid invoices do not get confused with recurring run rate. Deferred revenue reflects recognition timing. ARR reflects recurring contract value.

Contract structure also needs normalization. If a customer signs a multi-year agreement, ARR is the annual recurring portion of that contract, not the full contract value loaded into the first year. A three-year contract worth $360,000 in recurring subscription revenue contributes $120,000 of ARR, regardless of whether it was billed upfront or paid annually.

That distinction matters in growth reporting. Total contract value is useful for sales visibility and cash planning. ARR is the cleaner operating metric for comparing account value across different billing terms, expansion paths, and retention outcomes.

I usually prefer current-period MRR as the base for ARR when the subscription model is clean and pricing is stable. It gives leaders a present-tense run rate. That becomes even more important once you start measuring ARR movement in a waterfall, because churn, contraction, and recovered ARR only make sense if the opening base was calculated consistently.

Building Your ARR Waterfall From Start to Finish

Quarter-end closes, the board deck is due, and ending ARR is up. The first question is never the final number. It is why it moved, which levers drove it, and whether the gain is durable.

That is what the ARR waterfall is for. It bridges opening ARR to ending ARR with a set of movements your leadership team can act on. A good waterfall does more than summarize growth. It separates customer acquisition from account expansion, isolates contraction from full churn, and, if your billing stack supports it, shows which revenue was recovered before it became permanent loss.

The components that actually move ARR

Start with the movements you can defend at the customer level.

- Beginning ARR: The recurring revenue base at the start of the period.

- New ARR: ARR added from customers who became active recurring subscribers during the period.

- Expansion ARR: ARR added from existing customers through upgrades, added seats, add-ons, or recurring price increases.

- Downgrade ARR: ARR lost when existing customers reduce recurring spend but stay active.

- Churned ARR: ARR lost when customers cancel and leave the recurring base.

- Recovered ARR: ARR preserved or reinstated after a failed payment, cancellation intervention, or dunning and recovery workflow.

That last category is where many waterfalls fall short. In a standard model, revenue is either gained or lost. In practice, some revenue enters the at-risk bucket and then comes back. If your team uses recovery tooling such as Revcover, that saved revenue should show up as a positive movement in the waterfall, not disappear inside a smaller churn number. Otherwise, retention work looks weaker than it is, and finance loses visibility into how much ARR billing recovery is protecting.

A practical formula looks like this:

- Start with beginning ARR.

- Add new ARR.

- Add expansion ARR.

- Subtract downgrade ARR.

- Subtract churned ARR.

- Add recovered ARR, if the customer or subscription returned to the recurring base under your reporting policy.

- Arrive at ending ARR.

The policy behind recovered ARR matters. Some teams count recovery only if the subscription is restored in the same reporting period. Others count it whenever the account returns, then separately track gross churn and recovered churn. Either approach can work. What breaks reporting is switching logic quarter to quarter.

Sample ARR waterfall structure

| Component | ARR Value |

|---|---|

| Beginning ARR | Starting recurring revenue base for the quarter |

| New ARR | Annualized recurring revenue from newly active customers |

| Expansion ARR | Annualized gains from upgrades, add-ons, or price increases |

| Downgrade ARR | Annualized recurring revenue lost from plan reductions |

| Churned ARR | Annualized recurring revenue lost from cancellations |

| Recovered ARR | Annualized recurring revenue restored through billing recovery or successful save actions |

| Ending ARR | Beginning ARR plus gains minus losses, plus recovered ARR |

This structure forces cleaner operating discipline. Every movement needs a clear event, an owner, and a timestamp. Sales should not claim signed deals that have not gone live. Customer Success should not mix downgrades with cancellations. Billing operations should not bury payment recovery inside a generic retention adjustment.

Here is the trade-off I usually point out to growth and finance leaders. The simpler the waterfall, the easier it is to publish quickly. The more detailed the waterfall, the easier it is to diagnose problems early. For most SaaS teams, separating new, expansion, downgrade, churn, and recovered ARR is the right middle ground. It keeps reporting readable while preserving the operating signal you need to manage retention.

Once that structure is in place, the questions get better:

- Is net growth coming from acquisition, or are existing customers carrying the quarter?

- Are downgrades rising before logo churn shows up?

- Is recovered ARR offsetting an underlying billing issue that still needs fixing?

- Are gross losses acceptable, or is recovery masking preventable churn?

- Do your cohort trends line up with your churn rate calculation formula and reporting method?

One more rule keeps the waterfall credible. Do not include bookings, implementation-stage contracts, or future-dated starts before they enter the recurring base. ARR is a live run-rate metric. If the customer is not active under your policy, the deal belongs in pipeline, bookings, or committed ARR reporting, not in the current waterfall.

Done well, the ARR waterfall becomes the operating spine for revenue reviews. It shows whether the business is growing through healthy expansion, leaking through contraction, or retaining material ARR through recovery programs that deserve more attention.

How to Account for Churn and Recovered Revenue

Most ARR models handle gains and losses, but they still flatten churn into a single negative bucket. That's too crude for a retention-focused SaaS business.

Some revenue is gone because a customer made a deliberate choice to leave. Some disappears because the account downgraded to a lower recurring value. Some only looks lost because a payment failed, a card expired, or a cancellation flow gave the customer no meaningful alternative. If your reporting treats all of that as identical churn, you're missing operating signal.

Not all churn should be treated the same way

At minimum, ARR reporting should distinguish between two broad churn paths.

- Voluntary churn: The customer chooses to cancel.

- Involuntary churn: The subscription is interrupted because billing fails and the account isn't recovered in time.

That distinction affects what the business should do next. Voluntary churn usually calls for product, pricing, onboarding, or support intervention. Involuntary churn often points to billing operations, reminder timing, card update friction, and retry logic. If those causes are blended together, teams end up fixing the wrong problem.

A solid companion metric for this work is your churn rate calculation formula for subscription businesses. Churn rate tells you how much of the base you're losing. ARR movement tells you what that loss means in recurring revenue terms.

Where recovered ARR belongs in the waterfall

The standard waterfall needs an upgrade. In practice, many “churn events” are interrupted rather than finalized. A customer enters a cancellation flow, sees an alternative that fits better, accepts a pause or downgrade, updates payment details, or resolves a failed charge before the subscription dies. That revenue didn't just avoid loss in a vague sense. It was recovered.

Recovered ARR deserves its own positive line in the waterfall when your team can attribute it to a specific save or billing recovery action. Otherwise, the reporting understates retention work and overstates final churn.

A practical waterfall can therefore look like this:

| Movement type | How to treat it |

|---|---|

| New ARR | Positive contribution |

| Expansion ARR | Positive contribution |

| Recovered ARR | Positive contribution tied to saved or reinstated recurring revenue |

| Downgrade ARR | Negative contribution |

| Churned ARR | Negative contribution for truly lost recurring revenue |

Operator's view: If a customer was on track to leave and remained in the recurring base because of a successful intervention, that outcome should be visible in ARR reporting.

There's an important nuance here. Recovered ARR shouldn't become a vanity bucket. It needs a strict definition. Count it when a real at-risk subscription event would have reduced ARR and your team or system prevented that loss in a way you can audit. Don't count hypothetical saves. Don't count pipeline win-backs that haven't restarted billing. Don't count temporary holds unless your policy clearly defines when they remain active recurring revenue.

This framing also improves accountability. Growth can see whether save offers are preserving value. Billing ops can see whether payment recovery is preventing involuntary churn. Customer success can judge whether intervention paths are reducing preventable losses. Finance still owns the official policy, but operating teams finally get a number that reflects what they're influencing.

When recovered ARR is visible, churn reporting becomes less fatalistic and more useful. The question stops being “How much did we lose?” and becomes “How much was lost, how much contracted, and how much did we save before it left the base?” That's a much better lens for running a subscription business.

Handling Advanced Scenarios and Reporting Caveats

A quarter closes, the dashboard says ARR is up, and then Finance asks three uncomfortable questions. Did you annualize discounted ramp pricing at the promo rate or the steady-state rate? Did a paused enterprise account stay in the base? Did usage revenue spike because of true expansion or a one-off month? If those rules are not set before reporting, ARR becomes a negotiation instead of a metric.

Set rules before edge cases show up

ARR policy needs to be written down, owned by Finance, and reproducible by RevOps from billing data. If ARR is a board-level metric, the approval path should be clear too. The goal is simple. Two qualified operators should be able to pull the number independently and land on the same result.

Three scenarios usually create the most reporting drift:

- Discounted subscriptions: Decide whether ARR uses billed recurring value or list price. For operating reviews, billed recurring value is usually the cleaner choice because it reflects the revenue under contract today.

- Mid-period starts or plan changes: Define when normalized recurring value enters the base. Some teams count ARR once service is active at the contracted run rate. Others wait until the first full billing cycle. Either can work if applied consistently.

- Temporary pauses, credits, or save offers: Set a rule for when an account is still active recurring revenue versus when it has effectively left the base. This matters even more if you report Recovered ARR, because recovery only means something when the original risk state is clearly documented.

That last point creates a real trade-off. A generous save policy can preserve customers, but it can also blur whether ARR was retained, recovered, or never removed from the base in the first place. If you want Recovered ARR to be a useful operating metric, the handoff between churn risk, intervention, and reinstated billing has to be auditable.

Usage-based models need a normalization rule

Usage-based revenue creates the most debate because customer behavior is recurring, but monthly billings are not always stable. Annualizing a single strong month can overstate the run rate. Using too long a lookback can hide a real step-change in account value.

The right answer depends on how the business behaves. Teams with predictable usage patterns can justify a shorter normalization window. Teams with seasonality, overages, or customer-specific spikes usually need a broader averaging policy. What matters is that the method is fixed in advance and applied the same way every month.

This also changes how you read retention. A usage-heavy customer can stay active while contributing less recurring revenue over time. That will show up faster in revenue retention than in logo retention, which is why teams that track net dollar retention in SaaS usually spot contraction earlier.

Keep reporting layers separate

Billing systems should remain the source of truth for subscription status, contract value, and invoiced recurring charges. RevOps and recovery tooling can add context that billing platforms often miss, such as failed-payment recovery, cancellation deflection outcomes, and reinstatement attribution.

That distinction matters in practice. A tool like Revcover can support a positive Recovered ARR line in the waterfall when it prevents a cancellation or restores recurring billing after an at-risk event. It should not implicitly redefine the core ARR base on its own. Finance still needs a clean underlying ledger, and operators need recovery attribution on top of it.

Handled well, these caveats make ARR more decision-ready. Handled loosely, they turn every board deck, forecast review, and growth meeting into an argument about definitions.

Common ARR Calculation Mistakes to Avoid

Most ARR mistakes aren't math errors. They're classification errors, timing errors, and governance failures.

The mistakes that distort decision making

The first mistake is counting non-recurring revenue because it feels adjacent to subscription revenue. Setup fees, custom work, pilots, and one-time add-ons inflate ARR without improving predictability. That makes growth look stronger than the base really is.

The second mistake is ignoring contraction detail. Teams often celebrate new and expansion ARR while burying downgrades inside a broad churn bucket. That hides whether customers are leaving outright or shrinking their spend first. For a Head of Growth, those are different product and lifecycle signals.

The third mistake is terminology confusion. In SaaS, ARR means Annual Recurring Revenue. In traditional finance, ARR can also mean Accounting Rate of Return. That overlap causes real reporting issues. The SaaS CFO notes that this confusion can cause SaaS startups to misreport growth trajectories by an average of 18%.

If your metric definition changes depending on who's in the room, you don't have a reporting system. You have a vocabulary problem.

The policy test

A reliable ARR process passes a simple test.

- Can finance explain every inclusion and exclusion rule?

- Can RevOps reproduce the number from billing data?

- Can growth see how churn, downgrades, expansion, and recovery changed the base?

- Can leadership compare periods without changing methodology?

If the answer to any of those is no, the number is still fragile.

ARR becomes powerful when it's boring in the best way. Same rules. Same logic. Clear waterfall. Honest treatment of churn. Visible treatment of recovered revenue. That's what gives the metric operational value instead of just presentation value.

If your team wants clearer visibility into cancellation intent, save offers, failed-payment recovery, and the recurring revenue that gets preserved before it turns into churn, Revcover is built for that layer. It works alongside Stripe Billing, helps teams attribute recovered recurring revenue to specific interventions, and gives Growth, RevOps, and Success a cleaner picture of what's happening inside the ARR waterfall.